Amazon FBA Sales Tax Nexus Explained: The Part Amazon Handles, and the Part It Doesn't

The FBA Guys

April 11, 2026

Amazon FBA sales tax nexus became easier to misunderstand once Amazon started collecting tax in marketplace facilitator states.

That sounds backwards. It is not.

When the marketplace collects and remits sales tax on a transaction, the seller can start treating sales tax as a background platform function. The order comes in. The tax line appears. Amazon does what Amazon is required to do under the state's marketplace facilitator rules.

Amazon FBA sales tax nexus is the connection between your business and a state that can create sales-tax obligations. For Amazon sellers, the useful question isn't only whether tax was collected at checkout. The better question is which obligation you are actually talking about: collection, registration and filing, income or franchise tax exposure, or sale-readiness documentation.

Those get collapsed into one bucket constantly. The bucket is too small.

What Amazon Usually Handles Through Marketplace Facilitator Rules

Marketplace facilitator laws generally require large marketplaces to collect and remit sales tax on sales they facilitate for third-party sellers when the marketplace meets that state's rule. Amazon is the obvious example for FBA sellers.

The practical effect is simple enough: on many Amazon marketplace orders, Amazon is the party collecting and remitting the sales tax. That does a lot of work.

It doesn't answer every question.

The rules still vary by state, and state guidance changes. TaxJar's marketplace facilitator nexus table points out that thresholds and definitions differ, and that state laws and administrative rules can change. The Streamlined Sales Tax Governing Board also keeps a remote-seller/Wayfair FAQ that is useful precisely because the post-Wayfair environment is state-by-state, not one national rule you memorize once.

The mistake is treating the marketplace facilitator rule like a full tax department. It is one mechanism. It tells you who collected tax on a facilitated sale under a specific state's rule; it doesn't tell you whether your registration file is complete, whether a non-Amazon sale escaped the marketplace bucket, or whether a state notice is sitting in a mailbox nobody checks anymore.

That last part sounds small until diligence starts.

So where does that leave an Amazon seller?

With two files open, typically. Seller Central in one window and a state tax page or tax software dashboard in the other. Then a spreadsheet that has one tab called "nexus" and another tab called "do not touch," which is not a best practice so much as a confession that the seller knows the issue deserves a slower review. Nobody admits to the second tab. It exists.

Where Nexus Can Still Touch an FBA Seller

Nexus can come from different facts. Economic nexus is usually based on sales into a state. Physical nexus can come from physical presence, and inventory stored in a state can be part of that conversation.

That inventory point is why FBA sellers have historically worried about warehouse states. Your products can move through Amazon's fulfillment network without you choosing the building. The tax question then becomes awkward: you may know the customer state, but you may not have treated the inventory state like a compliance input.

What happens when a compliance issue comes from a place you didn't intentionally choose?

This is where the tax answer needs a CPA or SALT specialist. The article shouldn't pretend otherwise.

We have a pretty low tolerance for confident internet tax answers here. Inventory location, state thresholds, registration history, old sales channels, and entity structure can all change the answer. A seller with only Amazon marketplace sales has a different fact pattern from a seller who also ran a Shopify promotion, shipped wholesale orders to a reseller, and forgot about three manual invoices from last summer.

That is why the first pass should be factual, not emotional. Where did sales go? Where did inventory sit? Which channels collected tax? Which registrations already exist?

Here is the calmer operating rule: separate "Amazon collected on the order" from "we have checked whether the business has any registration, filing, income-tax, franchise-tax, or documentation obligations in that state."

Adjacent. Different files.

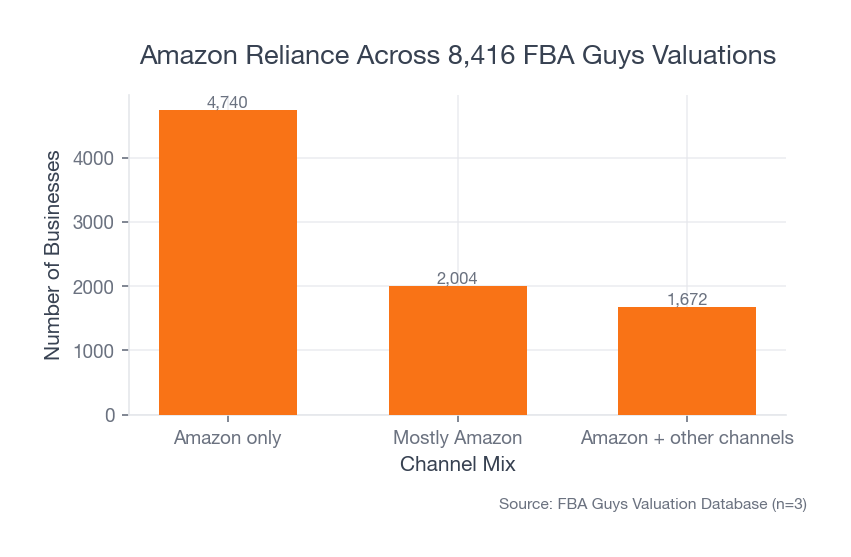

The Data Says This Is an Amazon-Heavy Problem

Among 8,416 successful valuations in our database, 4,740 were Amazon-only businesses and another 2,004 were mostly Amazon. That means 80.1% of submissions with channel data were either Amazon-only or mostly Amazon.

FBA is even more concentrated. Among submissions with fulfillment data, 6,076 were FBA and 1,944 used a combination of FBA and FBM.

So when we talk about nexus for this audience, we aren't talking about a tiny side channel. We are talking about the operating system for most of the businesses in the dataset.

Source: FBA Guys Valuation Database (n=8,416 successful valuations with channel data)

Source: FBA Guys Valuation Database (n=8,416 successful valuations with channel data)

The interesting part is what the database doesn't contain. It doesn't tell us whether a seller registered in California, filed a zero return in Washington, or ignored a notice that arrived at an old virtual mailbox address.

That absence matters. Buyers don't usually get nervous because a seller can recite a nexus rule from memory. They get nervous when the documentation trail is thin.

This is the part sellers underestimate. A clean answer with a caveat is easier to work with than a vague answer wrapped in confidence. "Amazon collected on marketplace orders, our CPA reviewed these three non-marketplace states, and this state remains open for review" is not perfect. It is traceable. That is usually the whole point.

A Practical Checklist Before You Register Anywhere

Start with the states where you have meaningful sales volume. Then look at the states where inventory may have been stored. Then look at non-Amazon channels, because marketplace facilitator collection on Amazon won't automatically solve Shopify, wholesale, Walmart, eBay, or manual invoice sales.

The state-by-state part gets ugly quickly. Some states use $100,000-style economic thresholds, some still use transaction counts, some treat marketplace facilitator sales differently for threshold purposes, and a few have odd local rules layered around the edges. This is why a clean checklist beats a heroic memory exercise.

There is also a sequencing issue. If you begin with "which states scare me?" you can end up with a noisy map and no decision. If you begin with "which states had meaningful sales, inventory, or registrations?" the map gets smaller. Not perfect. Smaller.

For an FBA seller, the question usually starts with three exports: Amazon marketplace tax collection, ship-to sales by state, and non-Amazon revenue by state. Which file gets weird first? Usually the second one, because it is where a wholesale invoice to Texas, six Shopify orders to Colorado, and a reimbursement booked as revenue can sit together as if they were the same kind of evidence.

That is not a tax scandal. It is a bookkeeping breadcrumb.

The non-Amazon channel is where this gets less tidy. Marketplace facilitator collection may cover the Amazon marketplace sale, but it doesn't magically reach back into a Shopify checkout, a wholesale invoice, a Walmart sale, or a manual order a seller pushed through because the buyer was "just one account." One account becomes five. Five becomes a tab called "other revenue." Then someone asks whether tax was collected correctly, and the room gets quiet for a reason that has nothing to do with the product.

Use this sequence:

- Export marketplace tax collection reports from Amazon.

- Pull revenue by ship-to state for Amazon and non-Amazon channels.

- Identify states where non-marketplace sales may cross economic nexus thresholds.

- Review whether FBA inventory creates any physical-presence questions.

- Check whether you are already registered anywhere and whether registration created filing obligations.

- Ask a CPA or SALT specialist before registering in a state just because a blog post made you nervous.

The last point deserves to sit by itself.

Registration can create work even when tax due is low. Some states expect filings once you are registered, including zero returns. A seller who registers everywhere "to be safe" can create a filing calendar that outlives the original anxiety.

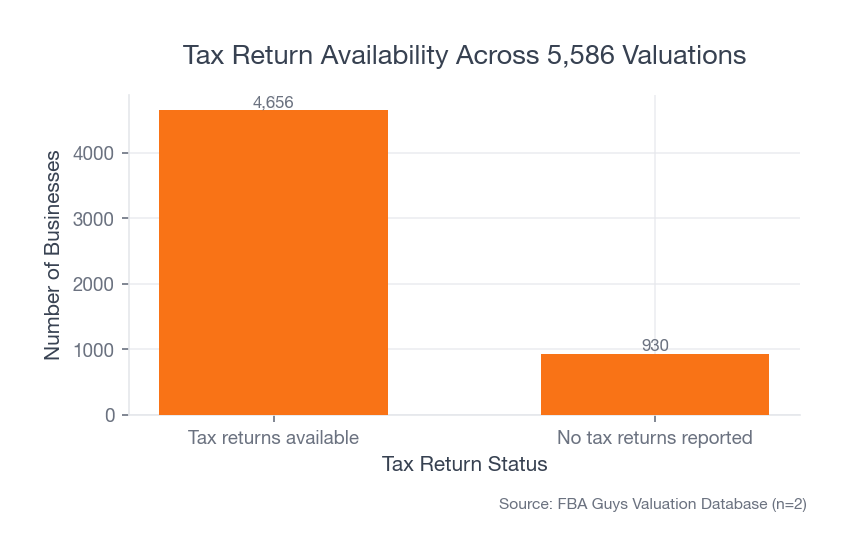

What This Means Before a Valuation or Sale

In our valuation database, 4,656 submissions with tax-return data reported having tax returns, while 930 reported no tax returns. The submissions with tax returns averaged a 5.94 confidence score; those without averaged 5.71.

That isn't a clean sales-tax finding. It is a documentation finding.

Source: FBA Guys Valuation Database (n=5,586 successful valuations with tax-return data)

Source: FBA Guys Valuation Database (n=5,586 successful valuations with tax-return data)

The implied valuation multiple gap was larger: 2.67 for submissions with tax returns versus 2.10 without them. We wouldn't hang a thesis on that alone, because tax returns are probably standing in for broader financial maturity. Better books, cleaner entity setup, fewer personal expenses floating through the P&L, a month-end close that doesn't require archaeology.

Still, the direction is not quite surprising.

Before a sale, the useful tax file is not a heroic memo. It is boring evidence: where you registered, what you filed, what Amazon collected, what your non-Amazon channels collected, who advised you, and what questions remain open.

The fact is, clean documentation makes uncertainty easier to price. Messy documentation makes small issues feel larger because the buyer has to wonder what else is hiding in the same drawer.

This is also where sellers can accidentally overstate certainty. "Amazon handles sales tax" may be directionally true for many marketplace transactions, but it is too blunt for a buyer trying to understand the risk file. A better answer names the boundary: Amazon handled collection on these marketplace orders; non-marketplace channels were reviewed separately; registration and filing positions were checked with an advisor; unresolved items are listed here.

That answer still may not be glamorous.

Good. Glamour is not what the buyer is buying.

FAQ

Does Amazon collect sales tax for FBA sellers?

For many marketplace orders, yes. Under marketplace facilitator rules, Amazon generally collects and remits sales tax on qualifying marketplace transactions where it is required to do so. The seller still needs to understand whether any registration, filing, non-Amazon sales, income-tax, or franchise-tax obligations remain.

Does FBA inventory create nexus?

Inventory can be part of a physical-nexus analysis, and FBA makes that uncomfortable because inventory can sit in states you didn't personally choose. The specific answer depends on the state and your facts, so treat this as a specialist question.

Should I register in every state?

Usually, that is a question for your CPA or SALT advisor, not a blanket operating rule. Registration can create filing obligations, including filings when no tax is due.

What should I keep for diligence?

Keep Amazon marketplace tax reports, sales by ship-to state, non-Amazon tax reports, registration confirmations, filing records, notices, and advisor memos. A buyer doesn't need a perfect story. They need a story that can be traced.

Closing

Amazon made the collection side easier in many states. It did not make the tax file disappear.

That is the strange part of Amazon FBA sales tax nexus now: the marketplace can handle the transaction-level tax while the business still needs a defensible record of what it checked, what it filed, and what it left to a specialist.

Curious what your business is worth?

Get a free, instant valuation and see how your Amazon business stacks up.

Get Your Free Valuation