Seller's Discretionary Earnings Explained: The Formula Is Easy. The Inputs Are Where Sale Price Moves.

The FBA Guys

March 27, 2026

Seller's Discretionary Earnings Explained: The Formula Is Easy. The Inputs Are Where Sale Price Moves.

Seller's discretionary earnings is the annual cash-generating power of an owner-operated business after you add back the costs the next owner would not inherit, and if you are wondering why this term keeps showing up in valuation conversations, that is because it is usually the number buyers use to decide what your Amazon business is worth in the first place.

That is the direct answer, but it still leaves out the part that actually costs sellers money. The formula is simple enough to fit on one line, yet the judgment calls underneath it usually are not. What belongs in earnings? What belongs in add-backs? Are your books reflecting the economics of the business, or just the month when the freight bill happened to land?

Across 8,563 valuations in our database with positive SDE and positive valuation estimates, the average implied multiple was 2.39x, which is another way of saying buyers are not paying a multiple of revenue and they certainly aren't paying a multiple of your best explanation. They are paying a multiple of earnings they believe will survive the handoff.

So what is seller's discretionary earnings, really, if you strip away the jargon?

It is the number that answers a blunt question you should care about long before you decide to sell: if one working owner takes over this business tomorrow, how much cash can the business actually throw off in a year?

SDE in Plain English

SDE starts with net income and then adjusts for owner-specific, discretionary, and non-recurring costs, which sounds tidy until you remember what a normal Amazon P&L looks like after a few years of growth, a rushed bookkeeper handoff, and one owner who has been treating the business card like a slightly more respectable personal wallet.

That matters because Amazon businesses often have books that are messier than the business itself. Owner payroll runs through the P&L. A one-time legal bill sits next to ordinary operating spend. Credit-card points drift into a personal account. There is a business class, an extra trip, a cleanup engagement with the accountant, and some oddly large "Meals" line item from a year the seller went to too many events. It all lands together, and you still need one earnings number a buyer can trust.

SDE is usually that number for owner-operated businesses because it gets closer to economic reality than raw net income does. If you want a calculator-first version, our SDE calculator handles the arithmetic, but it can't make the judgment calls for you and it won't rescue a lazy chart of accounts.

Why This Number Moves Sale Price So Hard

The first interesting thing in the data is that not every dollar of SDE gets treated the same way, and that is where a lot of simplistic explainer posts fall apart.

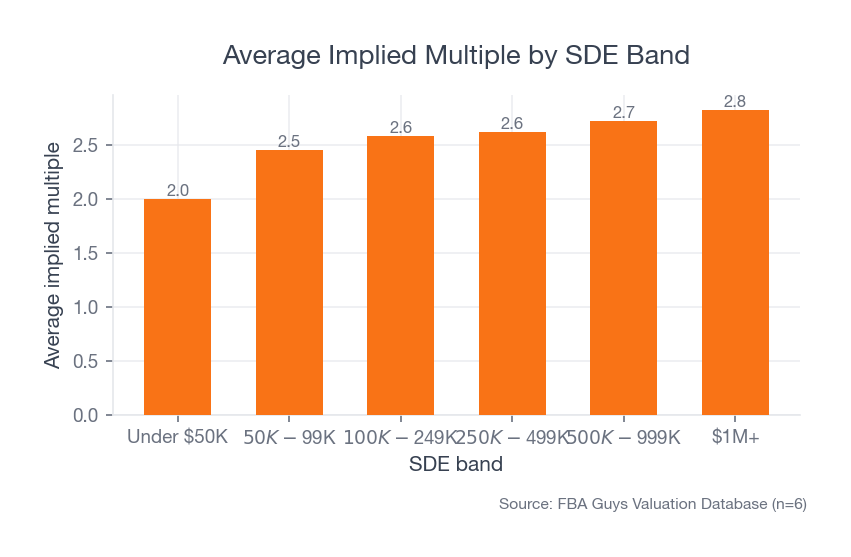

Businesses under $50K in SDE averaged a 2.00x implied multiple in our database. Businesses above $1M in SDE averaged 2.82x. Why does that matter to you if you are not selling this quarter? Because each extra dollar of credible earnings does two jobs at once.

Source: FBA Guys Valuation Database (n=8,563)

Source: FBA Guys Valuation Database (n=8,563)

Better SDE gives the buyer more earnings to buy, and it often improves the multiple attached to those earnings because larger and cleaner earnings usually feel more durable. That is a bigger deal than it sounds. If you understate SDE by $50,000, you do not just lose $50,000. You can lose that amount times the multiple, and if the understatement keeps your business sitting in a weaker earnings band, you may also lose the better multiple that stronger earnings could have supported.

If you want the broader context around how earnings flow into price, the full Amazon FBA business valuation guide goes deeper on the multiple side.

How to Calculate SDE Step by Step

The core formula is still this: Net Income + Add-Backs = SDE.

Start with net income, then add back one owner's salary, owner perks that do not transfer with the business, and one-time costs the next owner should not expect to absorb again. That sounds easy. It isn't. The Playbook's position here is worth taking seriously because it keeps surfacing the same expensive truth: proper add-backs can account for 10-30% of discretionary earnings.

That is not a cosmetic adjustment. It is the center of the exercise, and if you rush this section because the spreadsheet feels boring, you will usually end up with a number that looks precise and is still wrong.

Here is a simplified illustration:

- Net income:

$180,000 - Owner salary:

$70,000 - One-time legal cleanup:

$12,000 - Owner travel that will not recur:

$8,000 - SDE:

$270,000

Now run that business through the average implied multiple we see in the $250K-$499K SDE band, which is 2.62x, and the difference between sloppy and accurate SDE becomes about $235,800 in implied value. Same business. Different discipline. If you are wondering why experienced buyers get stubborn around this topic, that is why.

Before You Even Argue About Add-Backs, Fix the Accounting

This is the part people skip because it is less fun than talking about multiples, and honestly, it is also the part that makes the multiple conversation worth having at all.

For inventory businesses, timing can wreck the earnings number. A seller buys four months of inventory, prepays freight, books it on a cash basis, and suddenly the current period looks weaker than the business actually is. The operator knows the business did not become worse overnight. The buyer only sees a compressed SDE line and starts asking the wrong questions.

The Playbook is direct on this point. Cash-basis accounting can materially depress SDE for inventory-heavy businesses, while accrual accounting often gives a truer picture of what the company earned. If your bookkeeping still treats inventory timing casually, read this before you get cute with add-backs: accrual or cash accounting when selling your Amazon business.

For an hour the number can look broken, especially when you have a freight bill, a chunky inventory purchase, and a P&L that suddenly looks like the business forgot how to make money. Then you realize it is accrual timing, not business decay. That is a much cheaper problem to fix, but only if you are willing to admit the books need work before the valuation worksheet does.

Common Add-Backs. And the Ones Buyers Will Challenge.

Some add-backs are easy, or at least they are easy if you have the paperwork.

One owner's salary is usually easy. A one-time accounting cleanup is usually easy. A trademark expense is usually easy. Cash-back rewards on a business card that ended up in the owner's personal account are awkward, but still real. So is the education bill that helped the owner more than the next buyer. What makes buyers twitch is not the existence of add-backs. It is the feeling that the seller is trying to rename ordinary operating costs into seller perks after the fact.

The hard part is recurrence. If the expense keeps showing up, buyers will ask whether it is really discretionary. If you say product-launch costs are one-time but the brand survives by launching products on a regular cycle, that argument is weak. If the business depends on a premium office for employees to stay productive, that is not the same as the owner's vanity office. If your P&L has a line called "Amazon Misc" wobbling between $400 and $1,200 every month, nobody is going to assume the best, because that label usually means you stopped sorting before the buyer started reading.

Documentation wins here because narration does not, and you shouldn't want a valuation process that depends on speechcraft anyway.

SDE vs EBITDA for Amazon Businesses

Smaller owner-operated Amazon businesses are usually discussed in SDE, while larger and more management-run businesses drift toward EBITDA because the business is less about one owner's compensation and more about the operating machine.

If you still have a business where one owner is central to the workload, SDE is typically the cleaner first lens. Short section, on purpose, because the interesting work is not the acronym comparison. The interesting work is getting the earnings number right before you start arguing about which acronym makes you sound more sophisticated.

Why Margin and Trend Still Change the Answer

SDE matters because it anchors valuation. It doesn't finish valuation, and if you remember only one thing from this article, remember that.

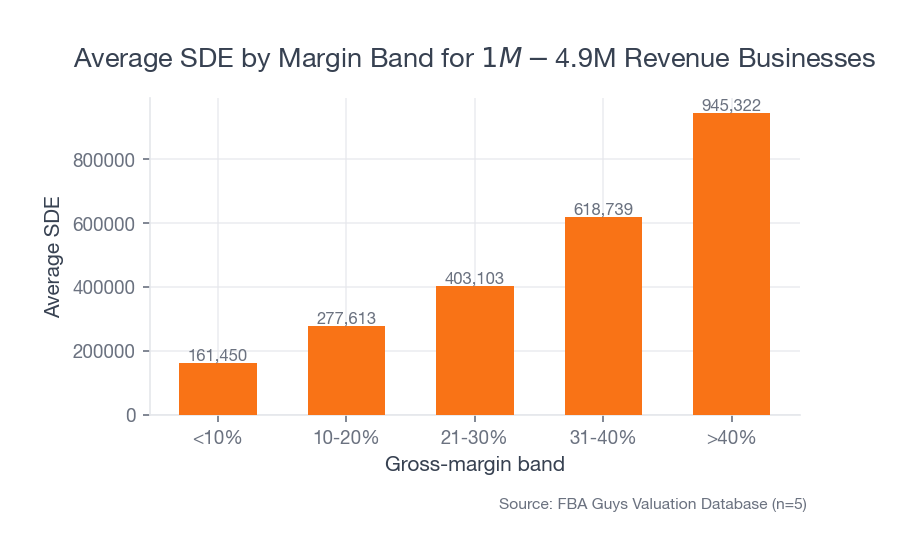

Our database makes that pretty clear. Businesses in the lowest gross-margin band averaged a 1.56x implied multiple, while businesses above 40% gross margin averaged 2.55x. In the $1M-$4.9M revenue band, the spread is even harder to ignore: the sub-10% margin group averaged $161,450 in SDE and $311,989 in valuation, while the >40% margin group averaged $945,322 in SDE and $2,764,269 in valuation. Same broad sales neighborhood. Completely different quality of earnings.

Source: FBA Guys Valuation Database (n=1,901)

Source: FBA Guys Valuation Database (n=1,901)

That is one reason we keep pushing sellers to understand more than top-line sales. Revenue can look healthy while earnings quality is quietly getting worse, and if you need a simpler warm-up metric, gross margin is a useful start. It just isn't the finish line.

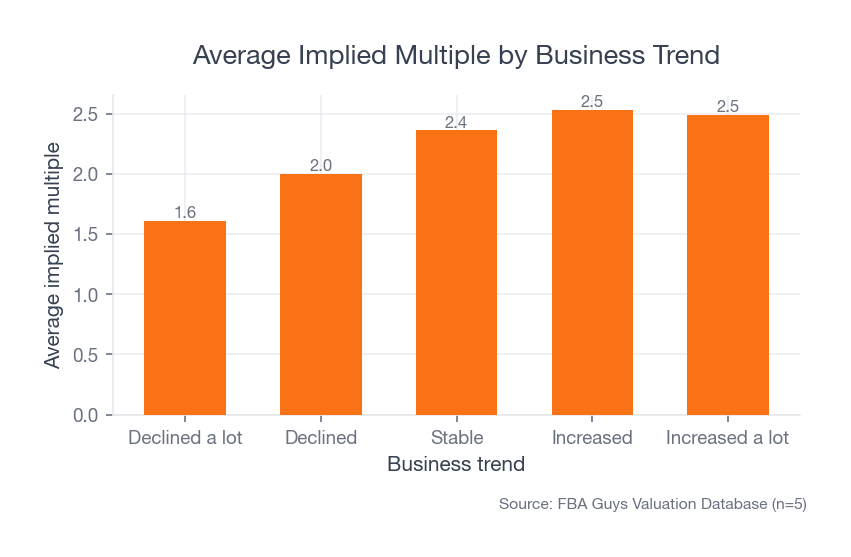

Then there is trend, which matters because buyers do not evaluate earnings in a vacuum. Businesses that had declined a lot averaged 1.61x. Businesses that were increasing averaged 2.53x. Interestingly, increased_a_lot did not beat ordinary increased by much in the aggregate, which is useful because it suggests buyers like growth, of course, but they like believable growth more than a dramatic spike they can't quite trust yet.

Source: FBA Guys Valuation Database (n=8,550)

Source: FBA Guys Valuation Database (n=8,550)

Treat SDE as the base number buyers start from, then ask the harder question you will eventually be forced to answer anyway: why should someone trust that number? Margin quality helps. Trend helps. Bookkeeping helps. If the earnings depend on one heroic owner doing three jobs, or on expenses stuffed into a mystery bucket, the multiple starts shrinking before the conversation gets comfortable.

FAQ

Can SDE be higher than net income?

Yes. It often should be in an owner-operated business, because SDE adds back legitimate owner-specific and non-recurring costs that net income leaves in place, and if it never rises above net income you should at least ask whether the books are leaving owner benefits buried in ordinary expense lines.

Is SDE the same as cash flow?

No. They are close cousins, not twins. Cash flow can swing because of inventory, debt service, taxes, or timing, while SDE is an adjusted valuation metric meant to show what one owner can actually take out of the business.

What documents make add-backs easier to defend?

A clean P&L, payroll records, invoices for unusual expenses, and enough support that the buyer does not have to take your word for it. If the add-back only works after a ten-minute monologue, it probably isn't a strong add-back, and if it only works after you explain away three years of messy categorization, it definitely isn't.

Does a higher SDE always mean a higher multiple?

Usually higher SDE helps, but no, not automatically. Weak margin, a declining trend, or ugly books can keep the multiple from moving the way you hoped, which is exactly why two businesses with similar revenue can still get treated very differently.

Why do some buyers still talk about EBITDA instead?

Because EBITDA fits larger businesses that already run more like operating companies than owner jobs. For most owner-operated Amazon brands, SDE is still the more useful first number, and if your business still depends on one owner to make half the decisions, it probably is the clearer one too.

Curious what your business is worth?

Get a free, instant valuation and see how your Amazon business stacks up.

Get Your Free Valuation