Amazon FBA Cost of Goods Sold Explained: Gross Margin Gets Too Much Credit

The FBA Guys

April 5, 2026

Most Amazon sellers can tell you their factory cost quickly.

Ask what actually belongs in cost of goods sold once freight timing, inventory turns, and the month a unit leaves the shelf enter the conversation, and the room usually gets quiet. The arithmetic is not the hard part. The hard part is keeping the number honest.

Amazon FBA cost of goods sold is the landed cost of inventory recognized when units sell. In practice, that means the supplier cost of the product plus the direct inbound costs required to get that unit into sellable inventory. It does not mean every Amazon expense you paid that month.

That sounds tidy.

It usually is not, because a flattering gross margin can coexist with heavy inventory, loose freight treatment, and books a buyer does not trust.

Amazon FBA Cost of Goods Sold Explained: The Short Version

If you want the useful version, not the textbook one, COGS for an FBA business should answer one narrow question: what did it cost you to put the units that actually sold into saleable condition?

That pushes you toward landed inventory cost, not just factory invoice cost.

So what belongs there? Start with supplier cost. Then include the direct inbound costs required to land that inventory. If you have unit-level prep or packaging costs that are part of getting that inventory ready to sell, they belong in the same conversation. PPC, software, payroll, and the rest of the account overhead do not belong there if your goal is to understand inventory economics rather than blur them.

If you want a cleaner distinction between gross margin and the rest of the income statement, our guide on how to calculate Amazon gross margin without fooling yourself is the natural companion read.

The reason sellers get tangled here is simple. Cash leaves before the units sell. Your P&L is trying to describe when earnings were generated, not when your card got hit.

What Actually Belongs in Amazon FBA COGS

Start with the product itself. Then move outward only as far as the direct landed cost of that inventory.

For most FBA operators, the cleanest mental model is this:

- Product cost from the supplier

- Direct inbound freight and related landing cost tied to that inventory

- Unit-level preparation or packaging cost required to make the unit saleable

- Recognition of those costs when the inventory sells, not when you happened to pay the bill

That last point is where the number breaks.

Sellers often know what they paid. They are much less certain which month should absorb it. Of course that sounds minor when you are ordering constantly. It stops sounding minor when you realize how easily a pretty gross margin can be assembled from timing noise.

And there is another trap here. Plenty of operators use "COGS" when they really mean "anything painful that came out of the account this month." That is not a definition. That is a stress response.

The operational bridge from COGS to landed cost matters here, which is why our Amazon FBA landed cost breakdown is a useful follow-on piece.

Why Freight Timing Breaks the Number Faster Than Sellers Expect

The Playbook uses a freight example because freight has no patience for vague accounting. A seller pays $24,000 in freight for the next four months of inventory, lists the business next month, and runs cash-based numbers. That move drags SDE down by the full $24,000 in the wrong month. On an accrual view, only one month of that freight belongs there. The other three months sit in the future.

And yes, that changes value.

In the same example, the corrected SDE is $18,000 higher and the business value is $63,000 higher at a 3.5x multiple. One freight bill. One month. Real money.

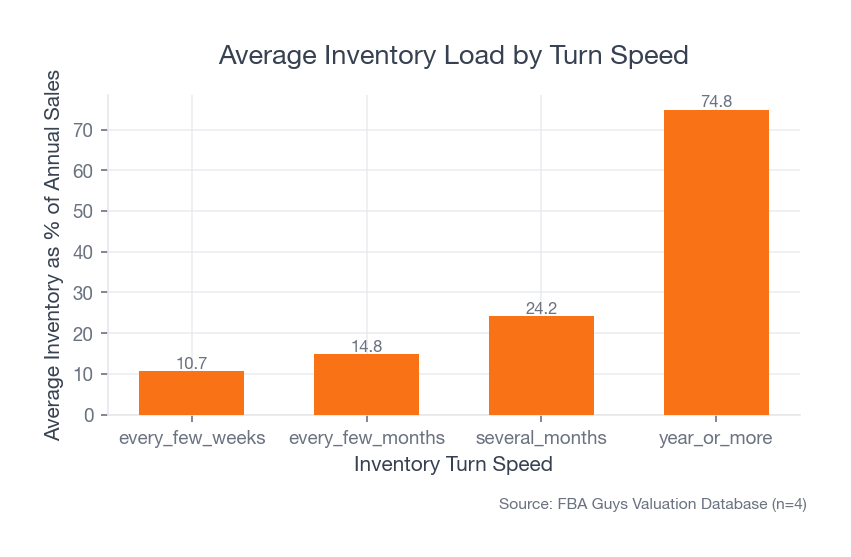

Our valuation database points at the same operating problem from a different angle. Businesses turning inventory every few weeks carry inventory equal to about 10.7% of annual sales on average. Stretch the turn cycle to every few months and the load rises to 14.8%. Push it to several months and it reaches 24.2%. Let inventory sit for a year or more and the average load jumps to 74.8% of annual sales.

Source: FBA Guys Valuation Database (n=4)

Source: FBA Guys Valuation Database (n=4)

Which one is easier to misread on a loose P&L?

The year-plus inventory business is not just slower. It is heavier. More cash is parked in stock. More freight winds up in the wrong month if the books are casual. More gross margin gets praised for doing less real work than the operator thinks.

If you are still managing this from an annual rollup, not a real monthly close, this is exactly where the Amazon seller profit and loss statement becomes more useful than another margin snapshot.

Gross Margin Gets Flattered When Inventory Accounting Gets Lazy

This is where the article gets a little irritating, because gross margin feels like clean evidence. It looks disciplined. It sounds precise. It is also rather easy to flatter if the inventory side of the business is doing ugly things out of frame.

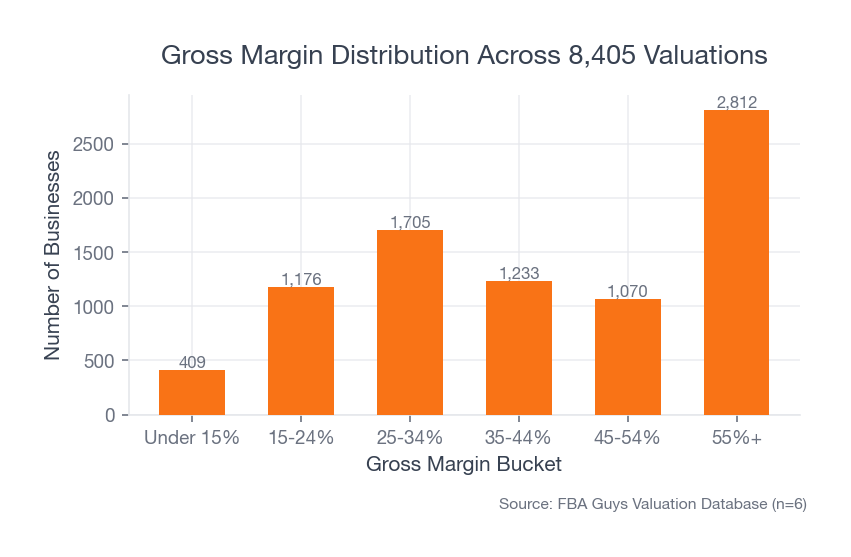

The database gives a useful warning. 2,812 of 8,405 successful valuations reported gross margin above 55%, which makes that the largest single margin bucket in the dataset. On its own, that sounds encouraging.

Source: FBA Guys Valuation Database (n=6)

Source: FBA Guys Valuation Database (n=6)

It is not enough.

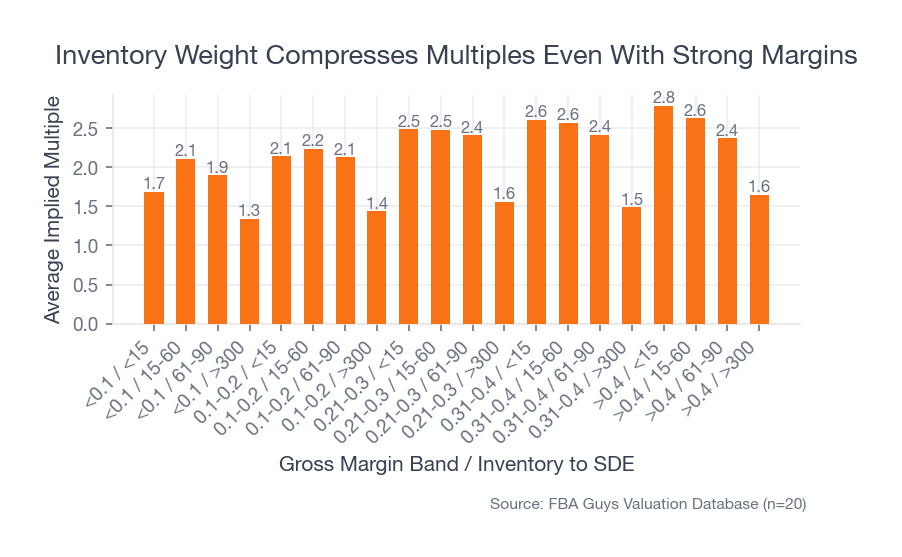

Among businesses with gross margin above 40%, the average implied multiple was 2.79x when inventory was less than 15% of SDE. Keep the same broad margin band but push inventory above 300% of SDE, and the average implied multiple falls to 1.65x.

Source: FBA Guys Valuation Database (n=20)

Source: FBA Guys Valuation Database (n=20)

Same margin story on the surface. Very different business underneath.

A buyer does not only inherit your margin. They inherit the amount of capital required to keep that margin alive. A business with attractive reported margin and ugly inventory weight can still be quite hard on the next owner.

One odd but important detour belongs here.

Slow-turn businesses are not all weak-margin businesses. Even in the year_or_more turn bucket, 173 businesses still reported gross margin above 40%. That is exactly why this topic matters. Attractive margin can hide heavy inventory drag rather well. If the margin line is the only thing getting attention, you can feel disciplined while the business gets heavier.

How to Track Amazon FBA COGS Without Building a Finance Department

You do not need a heroic finance stack.

You need a monthly process that makes the month believable.

The useful version usually does four things without fail:

- Reconcile what inventory was purchased

- Separate what sold from what is still sitting in inventory

- Carry freight and related landed costs with that inventory instead of dumping all of it into the payment month

- Review gross margin next to turns and inventory load, not by itself

That fourth step matters more than sellers think. Margin review in isolation is how you end up admiring a number that is only "good" because it borrowed from next quarter.

A short operating rule helps. If your gross margin improved, ask two follow-up questions before you celebrate: did turns improve too, and did inventory load stay sane? If either answer is no, the improvement may be cosmetic.

For an hour in one Playbook example, everyone thought there was a real integrity problem. An owner looked at a screen share, saw $297,000 in July revenue, and said there was no way the number was right. It turned out the books were the problem, not the screen. The bottom-line gap reached half a million dollars. Those are the moments when "close enough" accounting stops being a style preference and starts becoming a valuation problem.

If you need the broader operating backdrop, Amazon FBA accounting basics picks up where this one leaves off.

Why This Matters for Valuation, Not Just Bookkeeping

Buyers do not pay for attractive gross margin in the abstract. They pay for earnings they believe and working-capital demands they can live with.

The fact is, believable COGS is one of the quiet ways you make earnings believable.

Our documentation proxies are not a direct audit of bookkeeping quality, but the direction is clear enough to matter. Businesses with tax returns and separated books averaged a 2.75x implied multiple. Businesses with no tax returns and mixed books averaged 1.93x.

That does not prove COGS discipline alone created the gap. It does tell you the market rewards cleaner trust signals.

And this is where sellers get caught. They think COGS is a classification issue. Buyers experience it as an earnings-credibility issue and a working-capital issue. Those are not the same conversation.

Most operators do not need a prettier spreadsheet. They need a narrower definition, better timing discipline, and the willingness to look at gross margin next to the inventory burden that made it possible.

If you are trying to connect this back to sale value, our Amazon FBA business valuation guide is the next step.

FAQ

Is Amazon FBA cost of goods sold just the product cost?

No. If you stop at factory cost, you are usually understating what it took to land that inventory in saleable condition. The useful operating version of COGS is landed inventory cost recognized when the unit sells.

Why doesn't a high gross margin settle the question?

Because gross margin can still look strong while inventory gets heavy and turns get slow. In our database, even businesses above 40% gross margin saw implied multiples compress sharply when inventory load got extreme.

What is the biggest COGS mistake FBA sellers make?

Treating timing like bookkeeping trivia. Freight and other landed costs hit cash early, but they do not all belong in the month you paid them. If you expense them too soon, the margin line starts telling a cleaner story than the business deserves.

Does this matter if I am not planning to sell soon?

Yes. The sale conversation just makes the consequences easier to see. Long before a deal exists, bad COGS treatment can lead you to overstate margin, misread inventory performance, and make weak replenishment decisions.

External references worth checking:

- Amazon's Fee Preview report and related fee tools for current fee mechanics

- Amazon's Inventory Ledger report if you need a cleaner view of inventory movement

Curious what your business is worth?

Get a free, instant valuation and see how your Amazon business stacks up.

Get Your Free Valuation