Amazon Seller Profit and Loss Statement: The Monthly View Matters More Than the Annual Total

The FBA Guys

March 31, 2026

Most Amazon sellers can produce a number. Fewer can produce a believable one.

That sounds harsher than it should. But if you have ever watched someone pull a year-end profit and loss statement from bookkeeping software, feel relieved for twelve seconds, then realize freight landed in the wrong month, inventory never reconciled, and half the ad cleanup is sitting in a lazy "misc" bucket, you know the feeling.

An Amazon seller profit and loss statement should show monthly revenue, cost of goods sold, Amazon fees, advertising, operating expenses, and owner earnings in a way that reconciles to the bank, Seller Central, and inventory. For most product businesses, it should also be run on an accrual basis rather than cash if you want the statement to describe the business instead of the timing of your last reorder.

The harder answer is that a good Amazon seller profit and loss statement isn't just a tax document. It is an operating document and, eventually, a credibility document. You use it to decide whether the business is actually improving, whether the margin drop in September came from freight timing or weak pricing, whether ad spend is still buying something useful, and whether the business you think you own is the same one your records are quietly describing. Buyers use it to decide whether your earnings deserve belief.

What An Amazon Seller Profit And Loss Statement Should Include

At a minimum, the statement should let you see the business in monthly slices instead of one reassuring annual blob.

That means:

| Section | What belongs there | Why it matters |

|---|---|---|

| Revenue | Amazon sales, refunds, other channel sales if they exist | You need clean top-line visibility by month |

| COGS | product cost, inbound freight, packaging, prep, landed cost adjustments | Gross margin is fiction if COGS timing is wrong |

| Amazon fees | referral fees, FBA fees, storage, reimbursement offsets when applicable | Amazon takes money in several places. Pretending it is one line hides problems |

| Advertising | PPC spend, DSP if material, promo spend you want treated as recurring | Ad leakage changes owner earnings quickly |

| Operating expenses | payroll, software, bookkeeping, rent, 3PL, insurance, contractors | This is where pretty gross margins become ordinary businesses |

| Other income/expense | interest, one-time cleanup items, unusual charges | Keeps recurring earnings separate from noise |

| Owner earnings view | net income plus documented add-back schedule outside the P&L | Useful for valuation, but only if the base statement is clean |

Nothing exotic there.

The problem isn't that sellers know these categories exist. It is that the line placement gets sloppy in exactly the places that change decision-making. Freight lands in a random month. Inventory purchases get treated like current-period COGS. Amazon fees sit partially above and partially below gross profit. A reimbursement gets counted as if it fixed the root problem. Then somebody looks at the final line and calls it insight.

It isn't.

A usable Amazon seller profit and loss statement gives you a monthly story you can interrogate. Why did gross margin drop here? Why did ad spend jump there? Why did storage climb while revenue was flat? Why did the settlement report say one thing while the ledger implied another? If the statement cannot answer those questions without a second spreadsheet and a twenty-minute apology, it isn't doing its job.

Why The Monthly Amazon Seller Profit And Loss Statement Matters More Than Year-End Cleanup

This is where a lot of owners get too forgiving with themselves.

They assume the annual total is what matters. If the year ended profitably, the monthly mess feels like bookkeeping texture. Of course, buyers and lenders don't read it that way. They use the monthly view to see whether the business is stable, seasonal, distorted, or simply misunderstood by its owner.

The Playbook makes this point pretty bluntly. Monthly P&Ls that reconcile to the bank are part of the documentation baseline. It also uses a concrete example that should bother anyone still treating accounting method like a back-office preference: moving a growing product business from cash to accrual lifted SDE by $92,429, and at a 3.2x multiple changed value by $295,772.80.

Same business. Same operations. Different accounting method.

That is why the monthly view matters more than the annual total. The annual number can hide timing distortion. The monthly view exposes it.

And it exposes it in the exact places operators usually want to look away. Was the margin improvement real, or did inventory simply arrive later than usual? Did the ugly month come from actual demand softness, or did you true up freight, reimbursements, and ad charges all at once because nobody had cleaned the file in weeks? Did you really improve efficiency, or did the P&L just stop recognizing cost in the same month revenue was recognized? Those are not fussy accounting questions. They are operating questions disguised as accounting questions.

If you buy $80,000 of inventory in one month and almost none in the next, cash accounting can make month one look weak and month two look weirdly strong. An accrual view smooths that into the period where the inventory actually sold. That is not cosmetic bookkeeping. That is the difference between understanding your business and reading the mood of your checking account.

If you want the broader accounting-method argument, our piece on accrual or cash accounting when selling your Amazon business goes deeper. For this keyword, the shorter rule is enough: if your Amazon business carries meaningful inventory, your monthly P&L should usually be read on accrual.

Clean Books Change Value Faster Than Sellers Expect

This is the part sellers usually underestimate because documentation sounds boring right up until it starts changing money.

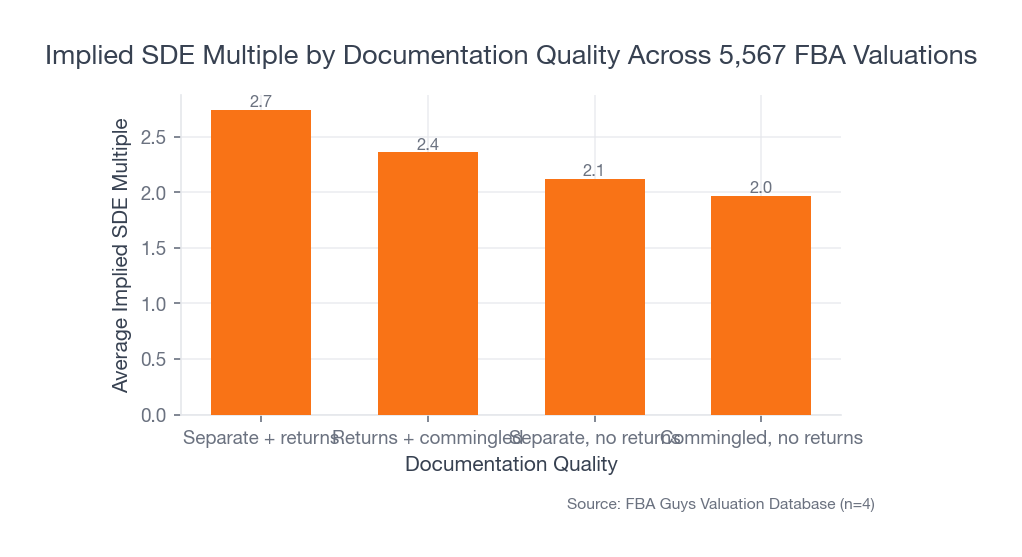

In our valuation database, businesses with separated structure plus filed tax returns averaged a 2.22x implied SDE multiple. Businesses with tax returns but commingled structure averaged 1.86x. Separated structure without tax returns averaged 1.81x. Commingled and no returns averaged 1.63x.

That isn't a rounding-error gap.

It is the market putting a price on whether your earnings can be trusted without a scavenger hunt.

Source: FBA Guys Valuation Database (n=5,567)

Source: FBA Guys Valuation Database (n=5,567)

If you only take one lesson from that table, take this one: a monthly Amazon seller profit and loss statement is part of your valuation architecture long before you ask for a valuation.

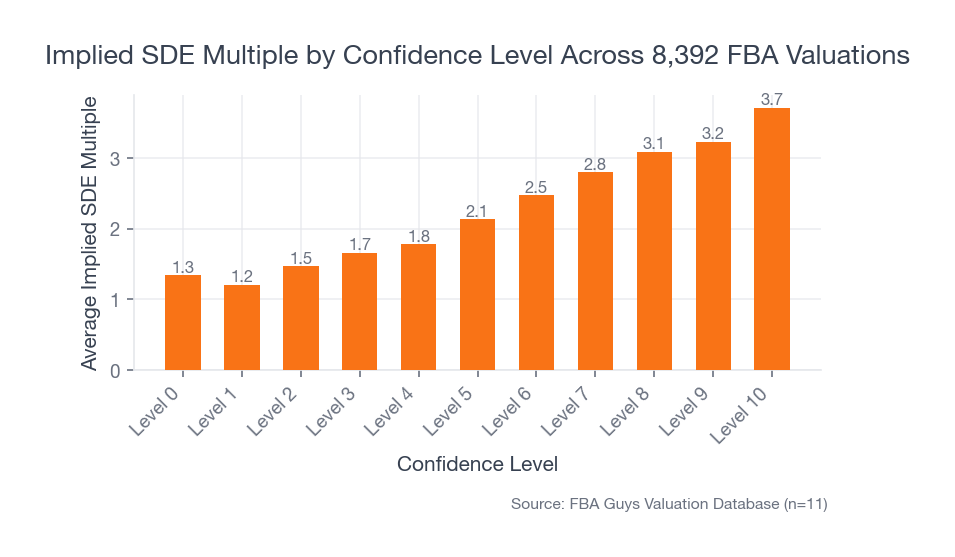

The confidence-score pattern says the same thing from another angle. In the database, level-5 confidence businesses averaged a 1.74x implied SDE multiple. Level 6 moved to 2.02x. Level 7 moved to 2.32x. Level 8 reached 2.58x. Level 10 hit 3.10x.

The fact is, the P&L isn't just reporting the business. It is helping decide how believable the business feels.

Source: FBA Guys Valuation Database (n=8,392)

Source: FBA Guys Valuation Database (n=8,392)

That matters long before you are thinking about a sale. If your monthly statement is built from separated accounts, filed returns, and reconciled reports, you can move faster operationally because you are not re-litigating the numbers every time something looks off. If it is built from partial exports, a few Excel patches, and memory, you spend half your time arguing with the statement instead of using it.

And what does that argument usually sound like? It sounds like "we know the year was good even if this month looks strange," or "that line always looks messy but it washes out by December," or "the accountant can explain it later." Maybe. But maybe the statement is telling you, rather plainly, that the business is more volatile, more inventory-hungry, or more loosely controlled than you wanted to admit. A good Amazon seller profit and loss statement doesn't flatter you. It narrows the places you can hide.

The Inventory Lines Usually Tell You Whether The Statement Is Honest

You can learn a lot from the inventory behavior that sits underneath a monthly Amazon seller profit and loss statement.

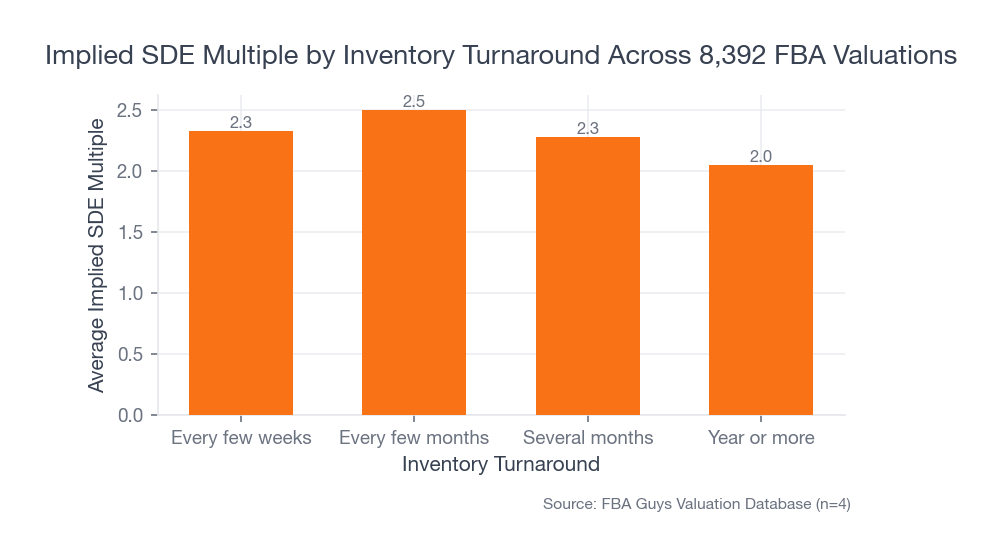

In our database, businesses turning inventory every few months averaged a 2.03x implied SDE multiple. Businesses turning every few weeks averaged 1.96x. That is close enough that it doesn't support some grand theory by itself. But once inventory sat for several months, the average multiple dropped to 1.82x. At a year or more, it dropped again to 1.63x.

That is useful because slow inventory can flatter a statement for a while. The gross margin might still look respectable. The revenue line might still look civilized. Meanwhile cash is getting pinned under aging stock, storage risk is drifting upward, and your monthly statement is quietly asking whether this business is earning well or merely postponing an argument.

Source: FBA Guys Valuation Database (n=8,392)

Source: FBA Guys Valuation Database (n=8,392)

This is also where stockouts matter. Among businesses in the database that reported inventory-stock behavior, those that never stocked out averaged a 2.14x implied multiple. Businesses that stocked out frequently averaged 1.63x.

No, that doesn't mean every stockout is a catastrophe. It means your P&L has to be read with the operating reality attached.

A monthly statement that shows margin but hides inventory drift is only half a statement. If you are reviewing the P&L without checking inventory aging, inventory on hand, and whether the Amazon settlement rhythm matches your cash assumptions, you are reading the attractive version of the business.

That version is popular. It just isn't very useful.

A Simple Amazon Seller Profit And Loss Statement Template

If you are trying to clean this up without rebuilding your whole accounting stack today, use a monthly template that stays boring on purpose.

- Revenue

- Refunds and returns

- Net sales

- Product COGS

- Freight and inbound shipping

- Packaging and prep

- Gross profit

- Amazon fees

- Advertising

- Payroll and contractors

- Software and tools

- Bookkeeping and professional fees

- Storage and 3PL

- Other operating expense

- Operating profit

- Interest, unusual items, and one-time cleanup below that line

- Net income

Then do one more thing that sellers skip constantly. Add a monthly note beside any line that changed because of something real: inventory receipt timing, major reimbursement, unusual legal bill, catalog cleanup, one-time agency work, whatever it was. The note can be short. It just has to exist.

Why?

Because a clean statement without context still creates stupid meetings. Someone sees margin dip in August, somebody else panics, and forty minutes later you discover it was a freight true-up tied to inventory that sold in September. Good records shorten that conversation.

Messy detail helps too. We have seen plenty of statements with a line like "Amazon Misc" swinging from $400 to $1,200 month to month. Nobody trusts that line. Nobody should. Rename it or break it out until a stranger could understand it without calling you.

If you need the profitability math underneath those lines, how to calculate Amazon FBA profit margin and how to calculate Amazon gross margin without fooling yourself are the right supporting reads.

What Buyers And Lenders Notice First

They don't start with your formatting.

They start with whether the statement feels coherent.

Can they follow revenue to gross profit without wondering where freight went? Can they see whether Amazon fees are being treated consistently? Can they tell whether inventory purchases are distorting the period? Can they match the monthly P&L to filed returns, bank activity, and supporting reports?

The Playbook is clear here too. In tighter diligence processes, buyers rebuild the profit and loss statement from underlying records. They aren't checking whether you own bookkeeping software. They are checking whether the story survives contact with documents.

That is why the monthly note beside an ugly line item matters more than people think. If October advertising looks bloated because you cleared a billing backlog, say so. If November COGS moved because a freight accrual was corrected, say so. If December is ugly because you wrote down stale inventory you should have dealt with in September, say that too. Buyers do not need a perfect business. They need a statement that behaves like it was maintained by adults.

That is why one of the worst habits in Amazon bookkeeping is year-end heroism. Sellers ignore the statement for ten months, panic in month eleven, push a bunch of fixes through, then act relieved because the annual total finally looks respectable.

Respectable isn't the goal.

Believable is the goal.

And honestly, operationally useful is the goal before that. A monthly Amazon seller profit and loss statement should help you decide whether to reorder, whether to trim spend, whether margin compression is temporary, and whether the business is getting more durable. If it only becomes readable after tax season, it is arriving too late to help run the company.

There is one more wrinkle here. Your P&L isn't your add-back schedule. Sellers blur those together all the time. The base statement should reflect recurring reality as cleanly as possible. Add-backs are a separate exercise used to explain owner-specific or non-recurring items when you move into a valuation context. If you want that bridge, seller's discretionary earnings explained is the better place to continue.

What To Fix This Month

If your Amazon seller profit and loss statement is shaky, don't start by redesigning the whole chart of accounts. Start smaller.

Run the last 24 months by month. Read it on accrual if inventory matters. Check whether gross margin behaves like a business or like a shipping calendar. Make sure Amazon fees are not scattered across random lines. Reconcile the statement to the bank and to Seller Central. Break out any lazy bucket that keeps moving just enough to avoid a real conversation.

Then ask the question that actually matters.

If a buyer, lender, or future version of you looked at this statement cold, would they trust it?

That is the standard. Not whether the year ended profitably. Not whether the accountant can explain it later. Not whether the software technically produced a report.

Would they trust it?

Because a good Amazon seller profit and loss statement does three jobs at once. It tells you what happened. It tells you whether the business is improving. And it tells the next serious reader that the numbers are worth treating as real. If your books can do that, the statement becomes useful every month instead of impressive once a year, and that is usually where better decisions start.

For current accounting software guidance and support docs, use your actual ledger system. For Amazon program mechanics that affect fee treatment, Amazon's own seller pricing documentation is the safer live reference than any static blog post.

FAQ

Should an Amazon seller profit and loss statement be cash or accrual?

For inventory-based Amazon businesses, accrual is usually the more useful operating view because it matches cost to the period where the inventory sold. Cash can be useful for literal cash planning, but it tends to distort business performance.

How often should I review my Amazon seller P&L?

Monthly. Quarterly is too slow if fees, ad spend, or inventory timing are moving around. Annual review is basically postmortem accounting.

What is the biggest mistake in an Amazon seller profit and loss statement?

Treating inventory purchases and landed cost timing casually. That one mistake can make a healthy business look weak or a weak one look healthier than it is.

Do buyers care about the P&L format or the underlying records?

Both, but the underlying records matter more. Clean formatting helps. Reconciled, believable support is what closes the argument.

Curious what your business is worth?

Get a free, instant valuation and see how your Amazon business stacks up.

Get Your Free Valuation