SDE vs EBITDA for Small Business: The Switch Happens Later Than Most Owners Think

The FBA Guys

April 1, 2026

There is a point where SDE stops being the right way to talk about a business and EBITDA starts doing a better job, but owners usually look for that point in the wrong place.

They look at revenue first, because revenue feels objective and grown-up and easy to repeat back in a meeting.

If you are trying to sort out sde vs ebitda for small business, the cleaner answer is this: use SDE when the owner's compensation, perks, and day-to-day role are still part of the economics a buyer is actually buying, and use EBITDA when management payroll is already a real operating expense and the business can be understood without pretending the owner is some separate species of labor.

That sounds clean enough on paper, but real businesses usually don't cooperate with clean rules.

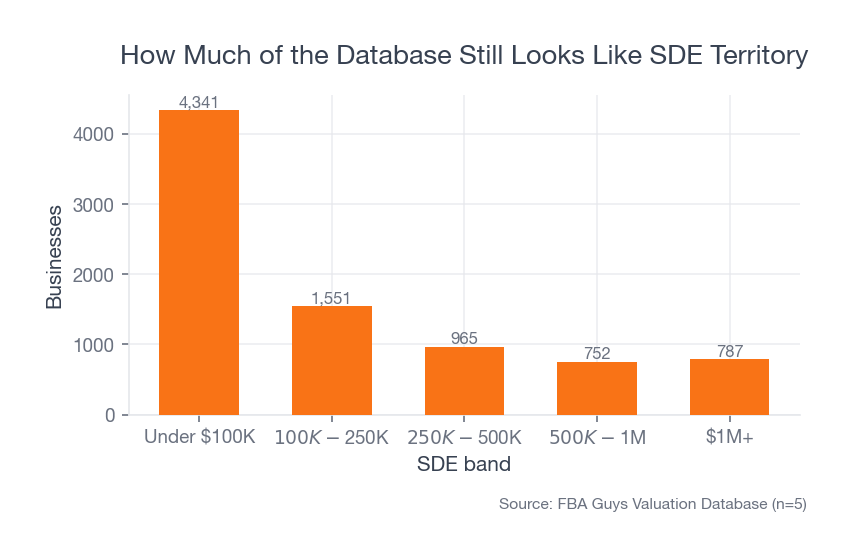

In the FBA Guys valuation database, 4,341 businesses sit under $100,000 in SDE. Another 1,551 fall between $100,000 and $250,000. Most of the database still lives in the zone where owner economics matter more than boardroom terminology.

Source: FBA Guys Valuation Database (n=8,396)

Source: FBA Guys Valuation Database (n=8,396)

That is why small business owners get themselves in trouble here. They hear that "serious" businesses use EBITDA and assume SDE is the kiddie table version. It isn't. It is the metric built for the situation they are actually in, even if they don't love how personal the answer feels once the owner's salary, perks, and actual workload are pulled into the light.

SDE vs EBITDA for Small Business: The Short Answer

SDE stands for Seller's Discretionary Earnings. In practice, it starts with net income and adds back the owner's compensation, owner-only perks, interest, taxes, depreciation, amortization, and one-time items that won't follow the business into the next owner's hands.

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It leaves owner compensation alone unless you are making a separate normalization outside the headline number, which is exactly why owners can talk themselves into using it too early.

SDE asks, "What does this business throw off for one owner-operator?" EBITDA asks, "What does this company earn before financing and accounting structure, assuming management costs are already where they belong?"

If you still need to normalize the owner's salary because the owner's role is inseparable from the business, you are usually still in SDE land. Why pretend otherwise?

Why SDE Usually Fits Small Owner-Operated Businesses Better

Most small businesses are not run by a management layer. They are run by an owner with a laptop, a bookkeeper they should have hired sooner, and a few expenses that become very interesting the second diligence starts, especially when the owner has spent two years calling those expenses "basically business development."

That is not an insult. It is small business.

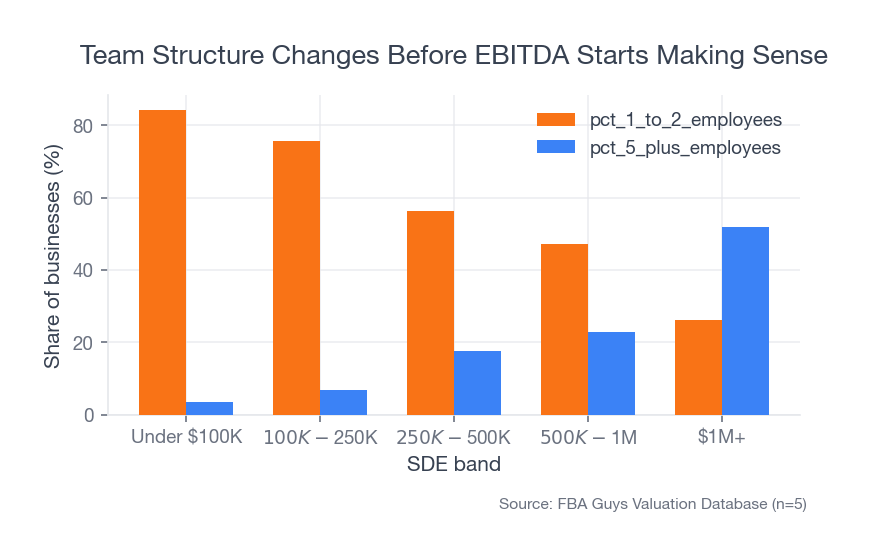

The database backs it up. Among businesses with employee-count data, 84.2% of the under-$100,000 SDE band have only one or two employees. Just 3.4% show five or more. That is not a profile where EBITDA gives you the cleanest picture. It is a profile where the buyer needs to know what the owner really took out of the business and what a replacement owner would actually inherit.

Source: FBA Guys Valuation Database (n=2,868)

Source: FBA Guys Valuation Database (n=2,868)

That is why the add-back schedule matters so much more than image management. If you need a refresher on that logic, start with Seller's Discretionary Earnings Explained, then come back, because this whole debate gets much less mysterious once you accept that you are trying to describe buyer economics rather than impress somebody with a cleaner acronym.

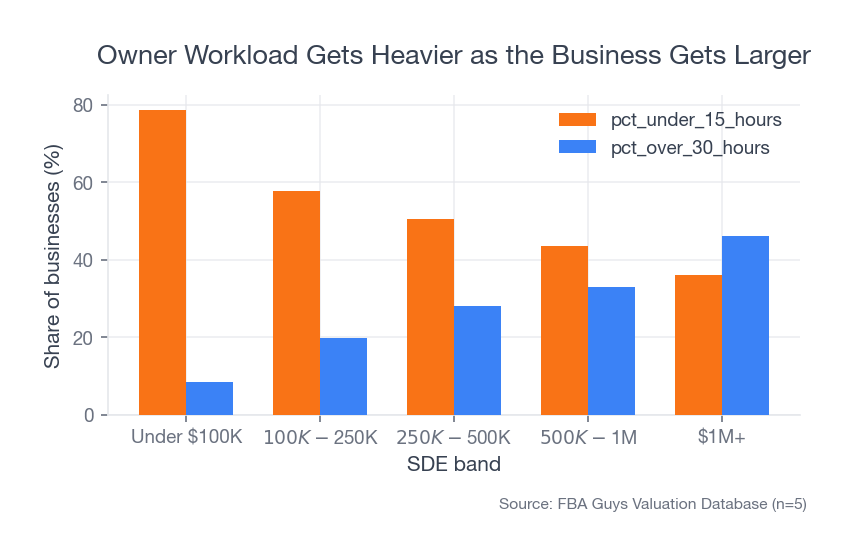

The same pattern shows up in workload. In the under-$100,000 SDE band, 78.6% of businesses report owner workloads under fifteen hours per week. Only 8.3% are over thirty hours. So even at the smaller end, you are not looking at a standardized corporate earnings stream. You are looking at owner economics arranged in different ways.

That is exactly what SDE is built to capture, and the fact is that EBITDA can make a small business look cleaner than it really is. Cleaner isn't the same thing as more accurate, and if you are the seller you should care much more about accuracy than cosmetics.

A composite that shows the problem

To illustrate: say a founder pays herself $140,000, runs a few personal travel charges through the business, and had a one-time legal bill tied to a trademark issue. If you jump straight to EBITDA, you are still stuck deciding what to do with the owner's role. With SDE, that question is not a side note. It is the point.

That is why buyers of smaller businesses still ask for the add-back schedule. They aren't being difficult. They are trying to see the actual engine, because if you don't show it clearly they will build a more conservative version on their own and make you live with it.

When EBITDA Starts Making More Sense

EBITDA becomes more useful when the owner is no longer the strangest expense on the P&L and when the salary structure already reflects what it would cost to keep the machine running after the owner leaves.

Once there is a real management layer, a finance lead, or a salary structure that already reflects market replacement cost, EBITDA starts to tell the cleaner story. You no longer have to keep asking whether the owner underpaid herself, overpaid herself, or treated the business checking account like a junk drawer.

The database does show movement in that direction as SDE rises. Among businesses with employee-count data, only 26.2% of the $1 million-plus SDE band still show one or two employees, while 51.9% show five or more. Average implied multiples also rise from 2.15x in the under-$100,000 band to 2.82x in the $1 million-plus band at current market conditions in this dataset.

But notice what didn't happen: the line didn't snap cleanly in half, and the database never gave us the satisfying handoff point people keep hoping to find.

Even in the $1 million-plus SDE band, more than a quarter of businesses with team-size data still look remarkably lean. That is the annoying answer people usually try to sprint past. Size pushes you toward EBITDA, but structure decides whether you are actually there, and you shouldn't hand buyers a cleaner story than the business can support.

If you are looking at valuation mechanics more broadly, the live pillar on Amazon FBA business valuation is the better next stop. This article is narrower. It is about the earnings lens, not the whole pricing model.

The Switch Is Not Revenue. It Is Replacement Management.

Owners keep asking whether the cutoff is $1 million in revenue, or $5 million, or some other round number that sounds confident on a podcast. We wouldn't use that rule, because revenue is a scale indicator and not a compensation logic.

The better question is whether management expense is already embedded in the business in a way that survives the owner's exit. If the owner still functions as operator, decision-maker, recruiter, inventory planner, and final approver on every meaningful move, EBITDA is usually flattering the business by pretending those responsibilities don't need a real replacement cost. Would you buy that story if you were wiring the money?

That is why the owner-workload data matters. Under-fifteen-hour workloads drop from 78.6% in the under-$100,000 SDE band to 36.1% in the $1 million-plus band. Over-thirty-hour workloads rise from 8.3% to 46.1%.

Source: FBA Guys Valuation Database (n=8,396)

Source: FBA Guys Valuation Database (n=8,396)

You can see the direction clearly, but you still can't reduce it to a revenue threshold without lying a little, and owners do this to themselves all the time. They hear "EBITDA" and think it upgrades the conversation. Sometimes it does. Sometimes it just hides labor that the buyer is absolutely going to price back in, which means the upgrade was mostly cosmetic.

What Amazon and Ecommerce Owners Usually Miss

Product businesses make this even messier because the books are often doing two jobs badly at once. They are trying to show operating performance and owner behavior in the same document, and those are not the same story when inventory timing, bookkeeping quality, and owner perks are all colliding in the same trailing twelve months.

That is one reason we keep circling back to clean SDE work in ecommerce. If your bookkeeping, accrual treatment, and add-backs are sloppy, EBITDA does not save you. It just moves the confusion into a more polished acronym.

For Amazon sellers in particular, this is why a clean seller profit and loss statement matters more than a premature fixation on "enterprise" framing. Before you worry about sounding bigger, you need to know whether your gross margin and your owner economics are even being measured honestly.

That sounds harsh, but it is still true, and most of the pain here comes from timing. Owners start worrying about EBITDA before they have finished doing the slower, less glamorous work of cleaning the books, documenting the add-backs, and showing a buyer what normal actually looks like.

How to Decide Which Number to Use in Practice

If the owner's pay, perks, and workload still need to be normalized, use SDE. If the business already carries a market-based management structure and the owner is not a special-case adjustment, EBITDA may be the better headline number.

If you are somewhere in the middle, which is rather common, calculate both. Then ask which one gives a buyer less room to invent their own story, because buyers will normalize the business one way or another and you don't want them doing that work in the dark.

That is the real test. Your job is not to win an acronym argument. Your job is to show the cleanest version of economic reality with the least hand-waving, and usually, for genuinely small businesses, that still means SDE.

FAQ

Is SDE the same as EBITDA?

No. SDE includes the owner's compensation and discretionary owner benefits in a way EBITDA usually does not, which is why the two numbers can feel close in one business and wildly different in another.

When should a small business use EBITDA instead of SDE?

When management payroll is already real, replacement cost is already in the P&L, and the business can be understood without turning the owner into a special adjustment. If you still have to ask what salary the owner should have been paid, you probably aren't there yet.

Is there a revenue cutoff where EBITDA becomes standard?

Not a reliable one. Revenue may point you in the right direction, but management structure is what actually decides it, which is a less satisfying answer and a much more useful one.

Which metric do buyers care about more?

They care about the one that explains the business honestly. For smaller owner-operated deals, that is usually SDE. For larger manager-run companies, EBITDA becomes more useful. What buyers don't care about is whether the seller picked the fancier acronym first.

If you are preparing a business for valuation, the better move is to get the P&L and add-backs right first, then worry about the label. The label matters. The mechanism matters more.

Curious what your business is worth?

Get a free, instant valuation and see how your Amazon business stacks up.

Get Your Free Valuation