Amazon FBA Cash vs Accrual Impact on Valuation: The Accounting Method Changes the Number Buyers Actually Price

The FBA Guys

April 27, 2026

The first strange thing about Amazon FBA accounting is how normal the wrong profit number can look.

You open the P&L. Sales are there. Amazon deposits are there. Inventory purchases are there too, usually in a month that looks nothing like the month when those units actually sold. The spreadsheet balances, the bank account reconciles, and the business still may be telling you the wrong story about what it earned.

Amazon FBA cash vs accrual impact on valuation comes down to one blunt point: valuation is based on earning power, and cash-basis books often measure payment timing rather than the profit generated by the inventory sold in that period. Accrual accounting lines up revenue with the costs required to produce that revenue. For an inventory business, that can change SDE, margin, buyer confidence, and ultimately the value range.

Seller's Discretionary Earnings, or SDE, is the profit measure most owner-operated Amazon businesses are valued from. A multiple is then applied to SDE. So a $50,000 error in SDE doesn't stay a $50,000 error for long.

At a 3x multiple, it becomes $150,000.

That is why this accounting question belongs in a valuation conversation, not only in a year-end tax conversation.

How Cash vs Accrual Changes an Amazon FBA Valuation

Cash accounting records money when it moves. Accrual accounting records income and expense when they are earned or incurred.

That sounds like an accounting-class distinction. It becomes much more interesting when inventory enters the picture.

An Amazon seller may pay a supplier in August, receive the goods later, and sell those units across October, November, and December. Cash-basis accounting can dump the inventory cost into August even though the revenue appears later. Accrual accounting holds that inventory cost on the balance sheet until units sell, then releases cost of goods sold into the P&L with the matching revenue.

That matching is the point.

Valuation work wants to understand recurring earning power. If the P&L shows a giant inventory buy in one month and artificially clean margins in another, the annual total may still look usable, but the monthly pattern gets noisy. The buyer or valuation model has to decide which months describe the business and which months describe timing.

The fact is, timing noise makes everyone work harder for the same answer.

That extra work matters because Amazon businesses already have enough noise. Fees come out before deposits land. Returns trail the sale. PPC spend can surge before the revenue shows up. Freight invoices arrive with their own sense of humor. Inventory commitments may reflect demand from three months ago, while the current P&L is trying to tell you what happened last month.

Then someone asks, "What did the business earn?"

You can answer that question from cash movement, but it will usually be a rougher answer than the valuation process wants.

Why Inventory Timing Distorts Cash-Basis Profit

Inventory makes cash accounting feel emotionally true. You paid the money. The bank account went down. Of course it feels like an expense.

The valuation question is different: when did the business consume that inventory to generate sales?

This is where cash-basis books can punish a growing Amazon business. A seller reinvesting into bigger inventory orders may look less profitable during the trailing twelve months because the P&L carries purchases for sales that haven't happened yet. In one inventory-business example, moving from cash-basis treatment to accrual treatment increased SDE by about $75,000. Another abbreviated P&L example showed a $92,429 SDE difference; at a 3.2x multiple, that was $295,772.80 of list-price movement.

Those aren't tiny bookkeeping footnotes.

They are valuation inputs.

The same timing problem can move the other direction. If the current period contains strong sales from inventory paid for earlier, cash-basis books can make the business look cleaner than it is. That creates a different problem. The seller may start believing a profit number that won't survive a proper accrual review.

Nobody enjoys that meeting.

The better habit is to make inventory follow the unit, not the invoice. If you want the operational version of that process, our guide on how to track COGS for Amazon FBA walks through the monthly close discipline behind it.

The SDE Problem

SDE is supposed to show the economic benefit available to one owner-operator before a buyer applies a multiple.

When COGS timing is wrong, SDE is wrong. Sometimes it is too low. Sometimes it is too high. The second case is less pleasant, because it can let a seller walk into diligence with a number that later collapses.

There is a scar here for anyone who has worked around owner-operated businesses long enough. Competent sellers build real companies while carrying books that lag behind the company they built. They are not careless. They are busy. The listing, the launch, the freight bill, the tariff change, the agency invoice, the weird Amazon reimbursement sitting in a suspense account for three months: all of it keeps moving.

Then valuation asks for one clean number.

This is why SDE and accounting method are tied together. You can't separate the multiple from the earnings base underneath it. A 3.2x multiple on a sloppy SDE number is just a tidy-looking answer built on a shaky input.

That is also why add-backs become more fragile when the base P&L is messy. Owner salary, one-time expenses, personal expenses, and non-cash items may all be legitimate adjustments, but they sit on top of the underlying accounting. If the cost of goods sold is floating around in the wrong month, the add-back schedule is doing detailed work on top of a number nobody fully trusts yet.

It is a bad place to be precise.

What Accrual Accounting Shows That Cash Accounting Misses

Accrual accounting gives you a cleaner read on gross margin, inventory consumption, and monthly profitability.

The FBA Guys valuation database does not contain a direct field saying which sellers use cash versus accrual accounting. That matters. We shouldn't pretend the data says something it doesn't say.

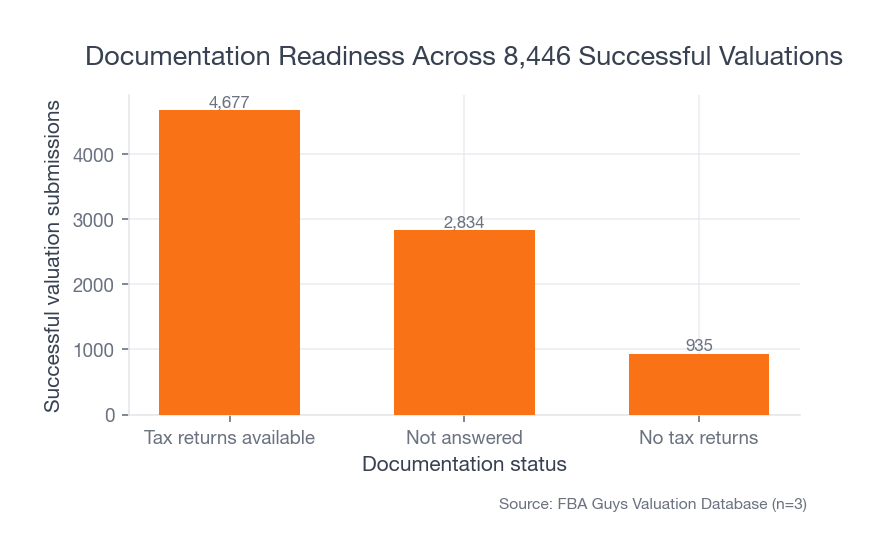

What the database does show is the shape around documentation and confidence. Among 8,446 successful valuation rows, 4,677 had tax returns available. Another 935 successful rows did not have tax returns available, and 2,834 did not answer the question.

Source: FBA Guys Valuation Database (n=8,446 successful valuation submissions)

Source: FBA Guys Valuation Database (n=8,446 successful valuation submissions)

The businesses with tax returns available averaged a $1,759,905 valuation and a 1.025 value-to-sales ratio. The successful rows without tax returns averaged $466,914 and a 0.860 value-to-sales ratio.

That is not proof that tax returns cause value. Larger businesses tend to have better documentation because they have to.

Still, the direction is useful. Better documentation tends to travel with more valuable businesses, and accrual books are part of the documentation stack that lets a valuation hold together.

Think about what a tax return actually represents in this context. It says the business has at least passed through a formal reporting process. It doesn't prove the books are perfect. It doesn't prove inventory was handled beautifully. It simply suggests the seller has moved beyond the "we can probably pull this together" stage.

For valuation, that stage matters.

Margin Is Where the Accounting Method Starts Talking

Margin is the place where this stops being abstract.

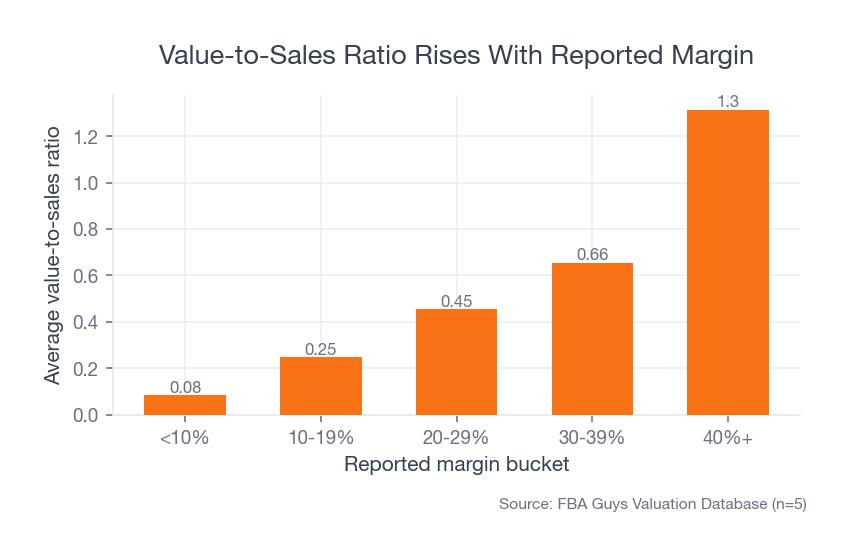

In the valuation database, successful submissions with under 10% margin averaged a 0.083 value-to-sales ratio. Businesses at 40%+ margin averaged 1.313. The values themselves reflect many factors, but the spread is hard to ignore.

Source: FBA Guys Valuation Database (successful submissions with reported margin data)

Source: FBA Guys Valuation Database (successful submissions with reported margin data)

If your accounting method moves COGS into the wrong month, the margin story starts moving too. One month looks dreadful. Another looks oddly clean. A buyer trying to understand the last twelve months has to decide whether the pattern is business performance, inventory timing, or a bookkeeper making one annual adjustment because monthly accrual accounting never happened.

That last one is more common than anyone enjoys admitting.

And it creates a second problem: trend analysis gets weaker. A business with improving margin should be able to show that the improvement came from pricing, sourcing, freight efficiency, ad discipline, product mix, or some other operating reason. If the books are cash-basis and inventory purchases are lumpy, the trend may be there, but it is buried under timing.

How much confidence should anyone put in that line?

This is where a seller can feel the difference between a clean Amazon seller profit and loss statement and a payment diary. The clean monthly P&L lets the business speak in patterns. The payment diary makes the owner explain every bump by memory.

Memory is a terrible accounting system.

When Cash Accounting Can Be Good Enough

Cash accounting can be fine for simple operating visibility when the business is small, stable, and not being valued for sale.

If you sell through inventory quickly, buy in modest batches, and aren't planning an exit, cash-basis reports may help you watch the bank account. Cash still matters. A profitable Amazon business can run out of cash if inventory turns, payment timing, and ad spend get away from it.

But valuation is a different use case.

The closer you get to a sale, a financing conversation, or even a serious internal valuation, the less patient the process becomes with rough accounting. "Close enough" starts asking for backup.

There is also a practical threshold. If inventory buys are small relative to monthly sales, cash-basis distortion may be mild. If you are placing large supplier deposits, carrying long lead times, importing product, splitting freight across shipments, or pushing growth with heavier inventory, cash-basis reports start losing the plot more quickly.

What if the business is seasonal?

Seasonality makes the question sharper. Cash-basis accounting can make the pre-season inventory build look painful and the selling season look unusually profitable, even though the business is simply preparing and then harvesting. Accrual accounting gives the season a cleaner shape. It won't remove seasonality. It will at least stop inventory timing from pretending to be margin volatility.

What Buyers and Valuation Models Need to Trust

A buyer is not only buying the products. They are buying the truthfulness of the financial history.

That sounds dramatic. It is rather practical.

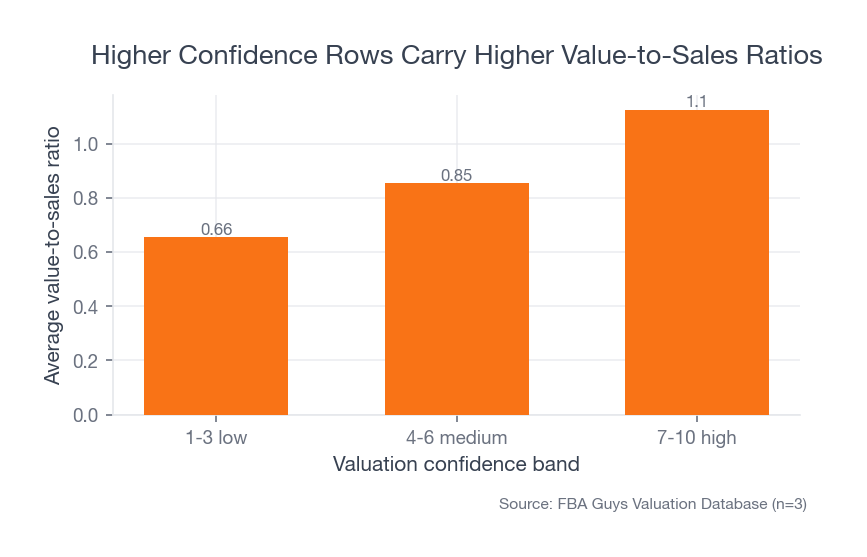

Among successful valuation rows with low confidence scores, the average value-to-sales ratio was 0.655. Medium-confidence rows averaged 0.854. High-confidence rows averaged 1.124. Confidence doesn't replace profitability, growth, risk, or transferability. It changes how much weight people can put on those inputs.

Source: FBA Guys Valuation Database (n=8,446 successful valuation submissions)

Source: FBA Guys Valuation Database (n=8,446 successful valuation submissions)

If the books require a long explanation before the profit number makes sense, the valuation starts absorbing that uncertainty. Sometimes through a lower number. Sometimes through more diligence. Sometimes through a deal that gets slower and less pleasant.

The mechanism is simple. A clean accrual P&L lets the reader spend more time evaluating the business and less time reconstructing the accounting. They can ask better questions: Are margins improving? Is ad spend efficient? Is the product mix getting stronger? Is growth translating into profit?

Messy cash-basis books pull the conversation backward.

Now the question is whether July margin was real, whether October COGS included a November shipment, whether the founder's card had personal expenses, whether the freight deposit belongs in inventory, and whether the last twelve months are actually measuring the last twelve months.

Nobody has priced the brand yet. They are still trying to find the floor.

How to Move Toward Accrual Without Making the Books Weird

Start with the monthly P&L. Run it by month for the last trailing twelve months and look at COGS as a percentage of revenue.

If the percentage jumps from 18% to 74% to 9%, you may be looking at inventory timing rather than margin reality. The answer is usually not a prettier spreadsheet. It is a bookkeeper who understands e-commerce inventory, landed cost, Amazon fees, freight, and the difference between tax cleanup and monthly management accounting.

This is also where a seller finds the messy detail that explains the whole problem: a freight invoice coded entirely to one month, a supplier deposit sitting in COGS before the inventory arrived, or an Amazon reimbursement bucket called "misc income" that includes refunds, replacements, and one $1,137.42 adjustment nobody wants to touch because it came through at 11:48 p.m. on the last day of the month.

Very normal. Very annoying.

A useful cleanup path usually looks like this:

- Separate the business bank and credit card activity if that hasn't already happened.

- Rebuild the last twelve months of monthly P&L detail.

- Move inventory purchases out of expense timing and into inventory until units sell.

- Track landed cost, not only supplier cost. Freight, duties, prep, and inbound costs matter.

- Reconcile Amazon deposits to the books instead of treating deposits as revenue.

- Keep an add-back schedule with source documents.

This is the unglamorous foundation behind Amazon FBA accounting basics. The tool matters less than the monthly discipline. QuickBooks, Xero, spreadsheets, exports, settlement reports, bank feeds: all of them can help, and all of them can still produce nonsense if the process is weak.

Should you wait until you are ready to sell?

Please don't. The best time to switch is before the trailing twelve-month period becomes important. If you expect a valuation next year, the books you are creating right now are already part of that future valuation.

That is the mildly irritating part.

The Practical Rule

Use cash to manage liquidity. Use accrual to understand performance.

Cash tells you whether the business can pay for inventory, ads, payroll, software, taxes, and owner draws without creating a panic. Accrual tells you whether the business actually generated profit from the units it sold. You need both views, but they answer different questions.

For valuation, accrual gets the heavier vote.

The reason is not that accrual accounting sounds more sophisticated. It is that valuation needs a durable earnings number. It needs SDE that can survive basic scrutiny, margin that isn't distorted by supplier-payment timing, and documentation that lets a buyer or valuation model focus on the business rather than the cleanup.

If the business may be valued, sold, financed, or benchmarked, the accrual version is the one that matters most. It gives SDE a better chance of being real, and valuation is only as solid as the SDE underneath it.

For a live valuation read, the Amazon FBA business valuation calculator is the place to start. For the accounting-method decision behind that number, accrual is usually the version that deserves the serious conversation.

FAQ

Does accrual accounting always increase an Amazon FBA valuation?

No. Accrual accounting can increase or decrease the number because it makes the profit measurement cleaner. If cash-basis books understated profit by expensing future inventory too early, accrual may increase SDE. If cash-basis books made recent months look cleaner than they were, accrual may reduce it.

That second possibility is worth taking seriously. A lower but accurate valuation is much better than a higher number that unravels later.

Is cash accounting wrong for Amazon sellers?

Cash accounting isn't automatically wrong. It is just limited. It can help you understand cash movement, but it is a weak way to measure inventory-based earning power when valuation depends on SDE.

Use it for liquidity if it helps. Don't ask it to carry the valuation argument by itself.

When should an Amazon seller switch to accrual accounting?

The earlier the better once inventory, freight, supplier deposits, and recurring valuation conversations enter the picture. At minimum, switch before the trailing twelve months you expect a buyer, lender, or valuation model to rely on.

Waiting until the business is already being evaluated turns an accounting improvement into a cleanup project. Cleanup projects create questions.

What is the first test for whether the books are accrual-ready?

Run monthly COGS as a percentage of revenue. If the ratio swings wildly without an operating reason, the books probably need accrual cleanup before the valuation number deserves much confidence.

Then check whether inventory, freight, duties, reimbursements, returns, and Amazon fees are being handled consistently. The boring details are usually where the valuation number starts getting more believable.

Can I use cash accounting for taxes and accrual accounting for valuation?

Possibly, depending on your tax situation and professional advice. Tax reporting and management accounting don't always serve the same job. For valuation, the important thing is that the financials used to calculate SDE reflect the operating performance of the business.

Ask a CPA for tax-method guidance. Ask an e-commerce bookkeeper to help build monthly books that explain the business.

Curious what your business is worth?

Get a free, instant valuation and see how your Amazon business stacks up.

Get Your Free Valuation