How to Value Inventory for Amazon FBA

The FBA Guys

April 19, 2026

Inventory is one of those numbers that looks solid until someone has to pay for it.

The units are sitting in FBA. The supplier invoices exist. The reorder spreadsheet has a neat column with cost per unit, freight, duties, and maybe a few notes from the last time the carton dimensions changed. On paper, it feels measurable.

Then a buyer asks a different question: which of this inventory is actually good, sellable inventory at closing?

If you want to know how to value inventory for Amazon FBA, start with this rule: value sellable inventory at landed cost, then separate that inventory value from the operating value of the business unless the deal specifically includes inventory in the purchase price. The business is usually valued from earnings. The inventory is usually paid for in addition to that value.

Usually.

That one word is doing some work, because inventory can change the deal conversation quickly. In the FBA Guys valuation database, successful valuation submissions with inventory reported an average inventory balance of $150,079. The same group averaged about $1.27 million in business value.

Those two numbers can live together comfortably. They can also become a problem.

How to Value Inventory for Amazon FBA

The clean version is simple:

Inventory value = sellable units on hand x landed cost per unit.

Landed cost means the full cost required to get the unit ready for sale. Product cost, inbound freight, duties, tariffs, prep, packaging, inspection, and any other cost that attaches to the unit before it is available to sell. We go deeper on the pieces of that number in our Amazon FBA landed cost breakdown.

Retail price doesn't belong in this calculation. Neither does expected profit.

If a SKU sells for $39.99 and costs $11.40 landed, the inventory value is built from $11.40. The buyer isn't buying your future margin when they reimburse inventory. They are reimbursing the capital already sitting in sellable stock.

There are three steps:

- Count only good, sellable inventory.

- Apply landed cost by SKU.

- Reconcile that number against Amazon, accounting records, and physical or 3PL stock.

That third step is where the work tends to hide.

Amazon's Inventory Ledger Summary View is useful because Amazon describes it as an end-to-end reconciliation report. It shows starting inventory balance, receipts, customer orders, customer returns, adjustments, removals, and ending balance. The report can be pulled daily, weekly, or monthly depending on the setup.

That doesn't give you a dollar value by itself.

The inventory value still has to come from your cost records.

Start With Sellable Inventory, Not Total Inventory

Total inventory is a lazy number.

Sellable inventory is the number a buyer can use.

There is a difference between 500 units in FBA and 500 units someone should pay for at closing. Some might be stranded. Some might be unsellable. Some might be in reserved status. Some might be seasonal stock that technically sells, but only after tying up cash for another eight months. Some might be an old packaging version that the listing photos quietly stopped matching.

This is the inventory list that matters:

- Fulfillable FBA inventory

- Inbound inventory that can be traced and is expected to arrive

- 3PL or warehouse inventory that is ready to ship

- Merchant-fulfilled inventory that is part of normal operations

- Sellable customer returns, if they are genuinely sellable

Then subtract the inventory that needs a different treatment:

- Unsellable or damaged units

- Stranded inventory

- Expired or near-expiring inventory

- Obsolete packaging or discontinued SKUs

- Excess stock beyond a reasonable operating level

Of course, "excess" is not a moral category. A business with long lead times may need four months of inventory to avoid going dark. A small, fast-turning accessories brand may look bloated with the same months on hand.

The question is not whether the inventory exists.

The question is what kind of capital it represents.

Use Landed Cost, Not Retail Value

Landed cost is the number that follows the unit.

If you paid $7.20 for the product, $1.85 for ocean freight, $0.62 in duties, $0.30 for inspection, and $0.43 for prep and packaging, the landed cost is $10.40. If there are 2,000 sellable units, the inventory value is $20,800.

That sounds tidy. It often isn't.

A messy detail: many real seller spreadsheets have one tab called "COGS," another called "Freight 2025," and a third that has the correct packaging cost only because someone updated it after a supplier changed carton count from 24 to 20. The math isn't complicated. The archaeology is.

This is why accrual accounting matters. If freight gets dumped into the month it was paid, the P&L can make earnings look lower in that month and higher later. For valuation, that can damage SDE. For inventory reimbursement, it can also understate the real cost sitting in stock.

If your COGS process is still being rebuilt, start with how to track COGS for Amazon FBA and Amazon FBA cost of goods sold explained. The inventory number gets much easier once the unit cost follows the unit.

The source material is blunt on this point: good, sellable inventory should usually be paid at landed cost. Not just factory cost. Not retail. Landed cost.

The fact is, a seller who tracks landed cost cleanly has a different conversation from a seller who says, "I think freight was around eight percent."

Why Inventory Gets Paid Separately From the Business

Most smaller FBA business valuations start with earnings:

SDE x multiple = business value

SDE means seller's discretionary earnings. It is the earnings of an owner-operated business after normalizing for owner compensation, add-backs, and non-recurring items. Our broader Amazon FBA business valuation guide covers the full valuation framework.

Inventory usually sits outside that formula. If the business is worth $900,000 and has $180,000 of good, sellable inventory, the buyer may pay $900,000 plus inventory. The inventory is not free working capital unless the deal says so.

This matters because "sold for 3x" can hide two very different structures.

To illustrate:

- Business A: $300,000 SDE x 3.0 = $900,000, plus $180,000 inventory.

- Business B: $300,000 SDE x 3.6 = $1,080,000, inventory included.

The headline multiple changed. The total dollars didn't.

That is one reason inventory-included listings can look more impressive than they are. The seller may feel better saying 3.6x. The buyer may feel better seeing 3.0x plus inventory. The wire amount can be identical.

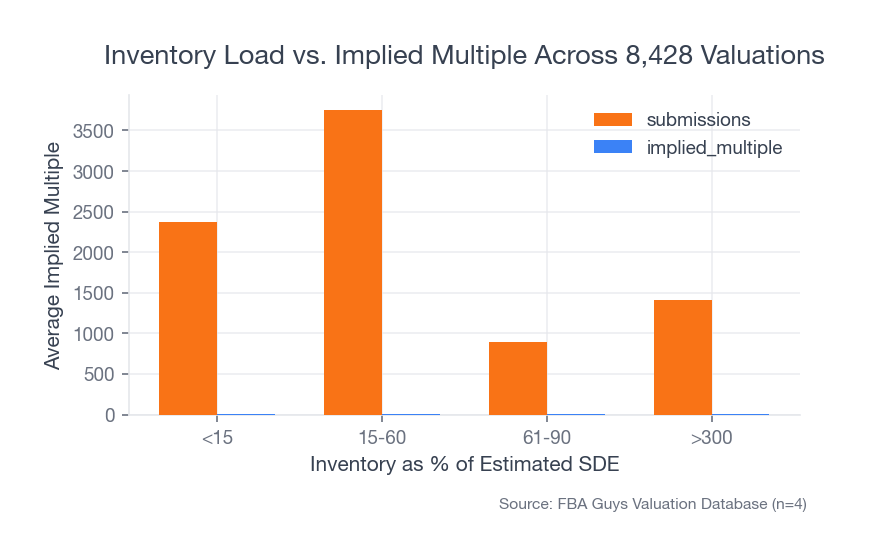

The Ratio That Changes the Conversation

The most interesting database pattern wasn't the average inventory balance.

It was the ratio.

Among 8,428 successful valuation submissions where we could estimate SDE, businesses with inventory below 15% of SDE averaged a 2.70x implied multiple. Businesses in the 15-60% band averaged 2.55x. The 61-90% group averaged 2.34x.

Then the floor moved.

Businesses with inventory greater than 300% of estimated SDE averaged a 1.54x implied multiple.

That doesn't mean inventory caused the lower multiple by itself. The database is not a courtroom. But the pattern makes sense operationally. When inventory gets too large relative to earnings, the buyer is not only buying a business. They are funding a balance sheet problem on day one.

Source: FBA Guys Valuation Database (n=8,428)

Source: FBA Guys Valuation Database (n=8,428)

A business with $700,000 in SDE and $100,000 in sellable inventory is one kind of conversation. A business with $200,000 in SDE and $600,000 in inventory is another. The second business may still be perfectly viable, but the buyer has to put more cash into inventory than the business produced in earnings.

There is probably a spreadsheet somewhere that makes that feel fine.

Cash doesn't always agree.

What Buyers Do With Excess Inventory

Excess inventory usually becomes a structure question.

If the business needs three months of inventory and the seller has four months, the buyer may pay for it cleanly. If the business needs three months and the seller has nine, the extra six months starts to look like seller financing, a discount, or a separate note.

The source material gives a useful example: a business sold for $1.1 million but had $600,000 of inventory. That is not a small add-on. The buyer would need $1.7 million total to buy a $1.1 million business, and much of the inventory was beyond the normal operating need.

There are fair ways to handle that. The buyer might pay cash for the amount needed to operate the business and use a short seller note for the rest. Or the parties may discount aged inventory. Or they may exclude obsolete SKUs entirely.

The seller's best defense is not argument. It is an aging report.

Show what is current, what is slow, what is seasonal, what is inbound, and what is dead. The more clearly the inventory is separated, the less likely the whole number gets treated as suspicious. If storage fees are already becoming part of the story, the split between normal carrying cost and excess stock shows up quickly. Our monthly vs. long-term FBA storage fee guide is a useful companion there.

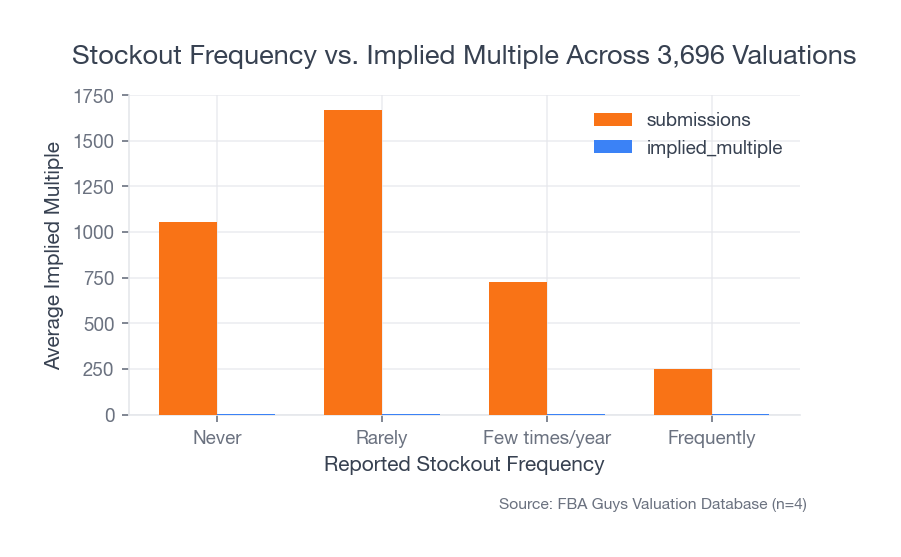

Stockouts Matter Too

Inventory that is too heavy creates one problem. Inventory that is too thin creates another.

In the valuation database, businesses reporting they never run out of stock averaged a 2.58x implied multiple. Those reporting rare stockouts averaged 2.50x. A few stockouts per year averaged 2.34x. Frequent stockouts averaged 2.00x.

Source: FBA Guys Valuation Database (n=3,696)

Source: FBA Guys Valuation Database (n=3,696)

This is the scar in the analysis. We expected the heavy-inventory penalty to carry the article. The stockout pattern made the article less tidy.

Lean inventory can look disciplined right up until it starts choking revenue. If a buyer sees repeated stockouts, the inventory valuation becomes part of a bigger operating question: how much working capital does this business really need to keep the sales line alive?

That question matters more than the inventory number by itself.

Reports to Pull Before You Value Inventory

Before you value inventory for an Amazon FBA business, pull the reports that make the number defensible.

Start with Amazon:

- Inventory Ledger Summary View

- Inventory Ledger Detailed View

- FBA Manage Inventory

- Reserved Inventory

- Stranded Inventory

- Inventory Health or aging view

- Inbound shipment records

Then pull your accounting and operating records:

- SKU-level landed cost table

- Supplier invoices

- Freight and duty invoices

- 3PL inventory reports

- Monthly accrual P&L

- Inventory aging report

- Reconciliation between book inventory and Amazon units

Amazon's FBA Inventory API can retrieve inventory summaries for all inventory, recently changed inventory, or specified seller SKUs. That is useful if your operation is connected through software, but the same principle applies manually: units and cost records have to meet.

Here is the practical test.

Could someone take your inventory valuation file, pick five SKUs at random, and trace each one from unit count to landed cost to current sellability without needing you to explain the whole business from memory?

If yes, the number is probably ready for a buyer conversation.

If no, keep working.

Closing-Date Inventory Is Its Own Number

There is one more detail that tends to get skipped until late in the process: inventory value at closing is not necessarily the same number you used at year-end, month-end, or in the first valuation estimate.

The business keeps moving.

You sell units after the first conversation. You receive inbound shipments. Amazon finds a few units, loses a few units, reserves others, and occasionally moves inventory between fulfillment centers in a way that makes the report look like it was written by a committee with no shared calendar.

So the closing inventory schedule needs a date.

Pick the measurement point, then reconcile to that point. If the parties agree inventory will be valued as of closing day, the inventory file should tie to closing-day units and current landed costs. If the deal uses a pre-closing estimate with a true-up, write down how the true-up works. This is not glamorous deal language. It saves arguments.

Tax inventory value may also differ from sale inventory value. That is a CPA question, especially if you are dealing with write-downs, obsolete stock, purchase price allocation, or inventory that has been treated differently on the books. Keep those conversations separate enough that one number doesn't accidentally pretend to do three jobs.

A Simple Inventory Valuation Worksheet

Use one row per SKU:

| SKU | Fulfillable units | Inbound units | 3PL units | Unsellable units | Landed cost/unit | Sellable inventory value | Notes |

|---|---|---|---|---|---|---|---|

| Example-SKU | 1,200 | 400 | 0 | 35 | $8.75 | $14,000 | 35 damaged units excluded |

The formula:

(fulfillable units + eligible inbound units + eligible 3PL units) x landed cost per unit = inventory value

Then add a notes column. Boring, yes. Necessary, also yes.

The notes column is where you explain the SKU with a packaging transition, the seasonal item, the unit with a supplier credit pending, the shipment Amazon has not fully received, and the discontinued color variant that still has 87 units sitting somewhere in FC transfer purgatory.

Those details don't make the business look messy. They make the inventory number look managed.

FAQ

Is Amazon FBA inventory valued at retail price?

No. For a business sale, good sellable inventory is typically valued at landed cost, not retail price. Retail price includes expected margin. Inventory reimbursement is about the capital already invested in the units.

Does inventory increase the valuation multiple?

Usually no. Inventory may increase total cash paid at closing, but it normally doesn't increase the SDE multiple. A listing that includes inventory inside the purchase price may show a higher headline multiple, even when the seller receives the same total dollars.

What happens to old or slow-moving inventory?

Old inventory needs a separate schedule. Some slow-moving inventory may still be sellable at landed cost. Some may need a discount. Some should be excluded. The aging report does the sorting.

Can I add back lost profit from stockouts?

Usually that is hard to support. Lost sales from stockouts involve assumptions about rank, conversion, demand, fees, and timing. A buyer may understand the story, but clean add-backs need math and logic that survive scrutiny.

What if my tax inventory value differs from my sale inventory value?

Ask your CPA. Tax inventory valuation, write-downs, purchase price allocation, and sale inventory reimbursement can overlap, but they are not the same job. A blog post shouldn't pretend otherwise.

Closing

Inventory valuation feels like accounting until the sale process begins. Then it becomes a trust exercise.

The buyer is asking whether the units are real, sellable, properly costed, and reasonable for the business they are buying. The seller is asking to be reimbursed for capital already put into stock. Both sides can be right.

The cleanest answer is still the simple one: count sellable units, apply landed cost, separate normal operating inventory from excess stock, and reconcile the number until it can stand without a long verbal defense.

That is how to value inventory for Amazon FBA without letting the inventory number swallow the business valuation.

Curious what your business is worth?

Get a free, instant valuation and see how your Amazon business stacks up.

Get Your Free Valuation