Amazon FBA Quarterly Tax Payments: The Calendar Is Easy. The Cash-Flow Discipline Is the Part Sellers Skip.

The FBA Guys

April 21, 2026

Amazon FBA Quarterly Tax Payments: The Calendar Is Easy. The Cash-Flow Discipline Is the Part Sellers Skip.

Quarterly tax payments sound administrative right up until they become personal.

An Amazon seller has a strong March. Inventory is already committed. PPC spend climbed because the rankings finally moved. Amazon sends the deposit, and for a brief moment the business feels rich. Then April 15 gets close, somebody opens the notes app, and the money that looked available turns out to belong partly to the IRS, partly to the next inventory order, and partly to the mistakes hiding in the books.

That is usually the real quarterly-tax problem. Not some exotic tax maneuver. Not a secret entity hack. Just a profitable business that started moving faster than the owner's reserve habit, and kept acting as if a strong Amazon deposit meant the cash was available for whatever came next.

Amazon FBA quarterly tax payments usually matter when you expect to owe enough tax that withholding will not cover it. For many self-employed sellers, that means estimated payments covering income tax plus self-employment tax. The IRS points people to Form 1040-ES, Publication 505, and the self-employed individuals tax center to decide whether payments are required and how to calculate them.

The dates aren't the hard part. The hard part is that Amazon businesses are built on deposits, fees, inventory timing, and month-to-month noise that makes taxable income less obvious than sellers want it to be. So the owner thinks they are late on a tax task when the business was actually late on bookkeeping.

Who Usually Needs Amazon FBA Quarterly Tax Payments

Not every seller does. A tiny store with losses, heavy startup costs, or enough withholding from another job may not need them yet. But how many sellers are really confused about quarterly taxes because the rules are exotic, and how many are confused because profitability arrived faster than the operating system around it?

The practical trigger is simpler than people make it sound. If the business is generating taxable profit and no one is withholding enough tax on the owner’s behalf, estimated payments usually become part of the operating calendar.

That is why sole proprietors, single-member LLC owners taxed the default way, and many partners run into this early. The profit flows through. The tax does too.

S corp owners aren't exempt from the conversation. They may have payroll withholding covering part of the year, but the pass-through portion can still leave the owner needing estimated payments if withholding is not enough. Sellers hear "S corp" and relax in a way the tax bill doesn't respect.

The 2026 Estimated-Tax Due Dates Are Exact Dates

For calendar-year individuals, the IRS currently lists these 2026 estimated-tax due dates:

- January 1 through March 31, 2026 income: due April 15, 2026

- April 1 through May 31, 2026 income: due June 15, 2026

- June 1 through August 31, 2026 income: due September 15, 2026

- September 1 through December 31, 2026 income: due January 15, 2027

The IRS FAQ on estimated-tax due dates and Publication 505 also note the weekend-and-holiday rule, plus the January exception when the return is filed and paid by the end of that month.

The thing sellers forget is that "quarterly" is just the nickname. The payment periods are uneven. June arrives faster than people expect, January carries farther than it looks, and Amazon cash flow adds its own distortion because a big inventory commitment can make a known tax date feel sudden anyway.

The Number You Need Is Not Revenue

Estimated tax is not based on gross sales. It is not based on Amazon deposits. It is definitely not based on the number you remember from Seller Central before fees, returns, ad spend, and inventory timing made everything less flattering.

It is based on expected taxable income.

That is what turns this into an accounting article whether the reader wanted one or not, because the seller who can't trust the year-to-date profit number doesn't actually have a tax-planning problem first. They have a measurement problem.

Amazon deposits hit net of fees, inventory is purchased before it sells, freight lands when it wants to, ad spend swells when a launch or ranking push is underway, and owner draws make the checking account feel healthier than the actual tax position. If the books are loose, the seller winds up trying to estimate tax from cash movement, which is how bad guesses get dressed up as planning.

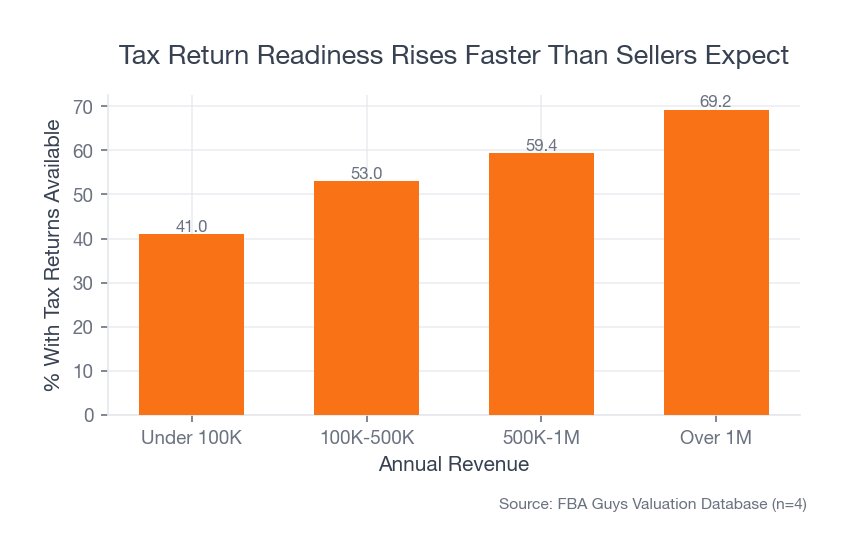

The Database Signal Is About Readiness, Not IRS Compliance

Our valuation database does not track who paid quarterly estimates on time. It does show a useful adjacent pattern: whether tax returns were available when businesses entered a valuation workflow.

The scale effect is not subtle:

- Under

$100Krevenue:41.0%had tax returns available $100K-$500K:53.0%$500K-$1M:59.4%- Over

$1M:69.2%

Source: FBA Guys Valuation Database (successful submissions grouped by revenue bracket)

Source: FBA Guys Valuation Database (successful submissions grouped by revenue bracket)

Separated finances barely moved in the same cut. That measure sat between 80.0% and 82.9% across all four revenue brackets.

That is the important interruption in the article. Sellers love the first administrative milestone. Separate bank account. Separate card. Clean enough.

Apparently not.

Basic separation is common. Full tax readiness lags behind it by a lot. That is exactly why quarterly payments feel easy in theory and sloppy in practice, and why a seller can honestly believe they are "organized" while still having no clean answer to a simple question like, "What did the business likely earn through May after the real costs are lined up?"

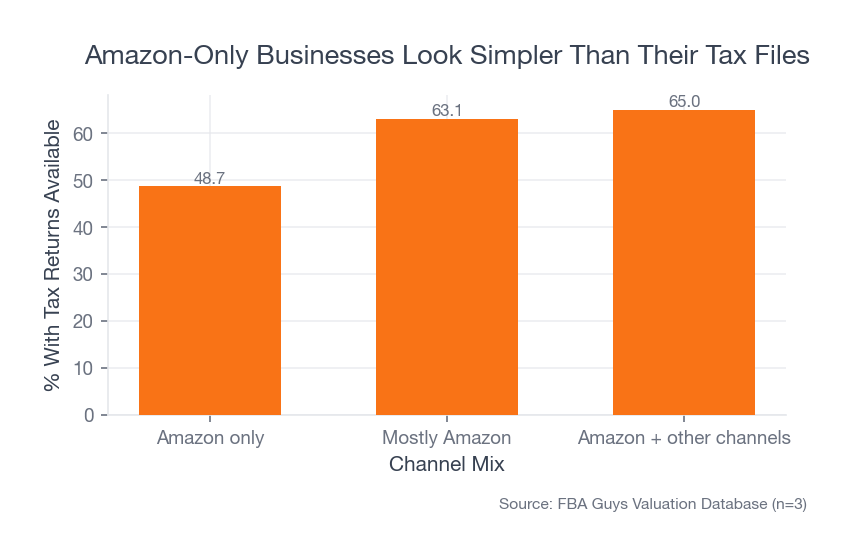

Amazon-Only Sellers Look Simpler Than They Are

This was the more revealing database cut.

Businesses marked as Amazon-only had tax returns available just 48.7% of the time. Sellers marked "mostly Amazon" were at 63.1%. Businesses selling through Amazon plus other channels reached 65.0%.

Source: FBA Guys Valuation Database (successful submissions grouped by channel mix)

Source: FBA Guys Valuation Database (successful submissions grouped by channel mix)

That does not mean mixed-channel operators enjoy taxes. It means complexity forces them to take the recordkeeping more seriously.

Amazon-only sellers can tell themselves a prettier story. Amazon tracked the sales. Amazon tracked the fees. Amazon issued the reports. So the tax workflow must be more or less handled.

It usually isn't.

Marketplace reporting is not the same thing as a reliable year-to-date profit picture, and it is definitely not the same thing as a payment plan.

How To Estimate Amazon FBA Quarterly Tax Payments Without Pretending You Know the Future Perfectly

Most sellers use one of two practical frameworks.

The first is the current-year estimate. Project the year based on what the business is doing now, update the estimate when the numbers change, and pay from that live forecast. Newer sellers often need this because the prior year is too small, too weird, or nonexistent.

The second is the safe-harbor framework described in Publication 505. Broadly, the required annual payment is generally the smaller of:

90%of the current year’s expected tax, or100%of the prior year’s total tax

For higher-income taxpayers, that prior-year number can step up to 110%.

This is useful for one reason above all the others: it separates penalty avoidance from perfect prediction. Sellers often freeze because they can't know the exact year-end number in April. Fair enough. The IRS didn't build the system around psychic certainty.

That does not mean you can guess blindly. It means you need a prior-year return, a live year-to-date P&L, and the willingness to re-estimate after margin, payroll, owner compensation, or ad spend changes materially.

Publication 505 also addresses situations where income subject to estimated tax starts later in the year. That matters for seasonal or newly profitable sellers. It is a timing rule, not a disappearing-act rule.

What if the business was flat in the first quarter and then woke up in late May? What if Prime Day planning pulled ad spend forward, but the actual profit snap happened later? That is exactly why sellers shouldn't lock themselves into one estimate in spring and never touch it again. The useful version is iterative: estimate, reserve, review, adjust, and then do it again when the business stops behaving like the version you budgeted against three months earlier.

The short operational version looks like this:

- Start with the prior-year return and the current year-to-date P&L.

- Estimate full-year taxable income, not gross deposits.

- Decide whether you are working off a current-year estimate or a safe-harbor target.

- Revisit the number after big shifts in margin, inventory, payroll, or owner comp.

- Move the reserve before the due date, not on the due date.

That list is less clever than most sellers want. It is also the version that survives contact with real books.

LLC, Sole Prop, and S Corp: The Entity Choice Does Not Replace the Habit

The entity conversation gets abused because sellers want one decision to solve three different problems.

If you are a sole proprietor or a single-member LLC taxed the default way, quarterly estimates are often just your problem at the owner level. Profit flows through, and if withholding is thin, you pay as you go.

If you elected S corp treatment, the mechanics change. You may have salary and withholding in the system already. You may also have owner profit that still leaves an estimated-tax gap. The election changes how the machine works. It doesn't eliminate the machine.

There is a reason LLC vs S corp for Amazon sellers keeps leading back to bookkeeping, payroll, and discipline instead of just tax-rate fantasies.

The readiness pattern in the database leans the same way. Sole props had tax returns available 75.1% of the time, LLCs 80.6%, and corp / S corp structures 91.8%. That doesn't prove the entity fixed anything. It suggests the businesses willing to carry more structure also tend to keep the tax file tighter, which is different and much less exciting.

The Mistakes That Trigger Penalties Are Usually Embarrassingly Ordinary

The classic errors are not dramatic.

Using revenue as the mental shortcut for taxable income. Forgetting self-employment tax. Treating Amazon deposits as fully spendable cash. Waiting until the due date to estimate the number. Assuming an S corp election solved the owner-level estimate. Assuming the CPA is calculating quarterly payments correctly from books the seller never finished cleaning up.

That last one deserves less respect than it gets. A CPA can work with imperfect books. They can't manufacture a clean quarterly estimate out of a vague P&L, half-categorized card charges, and inventory timing that is still being explained with hand gestures.

The playbook guidance behind this repo is blunt about the lane split: the bookkeeper keeps the monthly numbers right; the CPA uses those numbers for planning and filing. If the monthly P&L is not trustworthy, the quarterly-tax question is already downstream of a bigger failure.

What the Tax Reserve Should Feel Like

The reserve should feel mildly annoying.

If it feels painless, there is a decent chance you are under-reserving. If it feels impossible, the business may be drawing too aggressively, carrying inventory too hard, or misunderstanding what the real profit actually is. Either way, the reserve is supposed to create discipline. It is money you don't get to spend because the business already earned it for someone else.

That is where sellers talk themselves into trouble. They want the reserve to be temporary. They want to "borrow" from it for inventory just this once. They want the June payment to be lower because cash is tight, even though the profits that created the tax bill were real enough a month ago.

Don't make the reserve compete with operating cash in the same account if you can avoid it. Move it. Name the savings account something unromantic. Let it sit there being irritating. That irritation is better than acting surprised every time a due date lands exactly where the IRS said it would land.

What a Working Quarterly-Tax Rhythm Looks Like

This part is not glamorous, which is why it works.

Close the books every month. Review year-to-date profit instead of deposits. Move the tax reserve into a separate savings bucket before it starts pretending to be inventory money. Re-estimate after big changes in margin, payroll, owner compensation, or channel mix. Ask the CPA to review the method before the due date, not after the penalty notice.

If you have W-2 income somewhere else, revisit withholding there too. Sometimes the simplest fix isn't four larger estimated payments. It is better withholding in a system that already exists.

And if the numbers are still too fuzzy to estimate cleanly, the next move isn't reading one more tax explainer. It is fixing the accounting.

That is where Amazon FBA accounting basics, the monthly discipline in an Amazon seller profit and loss statement, the entity discussion in LLC vs S corp for Amazon sellers, the deductions cleanup in Amazon seller tax deductions, and the professional-role split in Do I Need a CPA for My Amazon Business? start being more useful than another calendar reminder.

The calendar is easy. The part that gets sellers is building a business that knows what the payment should be before the deadline arrives, and then being willing to leave that money alone once they know.

FAQ

Do Amazon sellers have to pay quarterly estimated taxes?

Some do, some do not. It generally depends on whether expected tax will exceed what withholding and credits cover. Many profitable self-employed sellers wind up needing estimated payments.

What are the 2026 quarterly tax payment dates?

For calendar-year individuals, the current IRS due dates are April 15, 2026; June 15, 2026; September 15, 2026; and January 15, 2027, subject to weekend or holiday adjustments.

Does an LLC change quarterly tax payments?

Not by itself. A default-taxed LLC usually still leaves the owner handling estimated payments personally.

Does an S corp mean I stop making estimated tax payments?

No. Salary withholding may help, but owner-level estimates can still be needed if the withholding is not enough to cover the full tax picture.

What is the biggest quarterly-tax mistake Amazon sellers make?

Treating Amazon deposits like profit, then treating profit like cash that can be spent before a tax reserve is carved out.

Curious what your business is worth?

Get a free, instant valuation and see how your Amazon business stacks up.

Get Your Free Valuation